Wind Mitigation Inspection in Miami: Your Guide to Insurance Savings

The $150 Miami Inspection That Saves You Thousands Every Year

A wind mitigation inspection is probably the highest-ROI $150 you can spend as a Miami homeowner. Pay for the inspection once, file the OIR-B1-1802 form with your insurance carrier, and you unlock 10 to 45 percent off the wind portion of your annual premium. On a typical Miami home with a $5,500 annual premium, that's $800 to $2,000 per year in savings, every year, for as long as you own the home.

I tell every client to get this inspection done within 6 months of any new roof installation, and ideally right after. Most Miami homeowners don't know the inspection exists, don't know how to find a qualified inspector, and don't know which credits they qualify for. As a result, they're paying full price on insurance when they could be saving thousands.

Here's exactly how wind mitigation inspections work in 2026, what credits each roof feature unlocks, and how to make sure you capture every discount you're entitled to.

What Is Wind Mitigation?

Wind mitigation refers to features of your home's construction that reduce damage risk during hurricanes and high-wind events. Florida insurance companies are required by law to offer discounts for homes with specific wind-resistant features. but you must prove these features exist through a certified wind mitigation inspection.

Why Wind Mitigation Matters in Miami

Hurricane Exposure : Miami sits in one of the nation's highest hurricane risk zones. Insurance companies charge premium rates to cover this risk. unless your home has features that reduce damage likelihood.

Significant Savings : Average Miami homeowner saves $400-$1,200 annually with full wind mitigation discounts. Over a 30-year mortgage, that's $12,000-$36,000 in cumulative savings.

Required Documentation : Insurance companies won't apply discounts without official OIR-B1-1802 wind mitigation form completed by licensed inspector.

Home Value Protection : Beyond insurance savings, wind mitigation features actually protect your home during storms, reducing repair costs and property damage.

Learn about complete roof protection for Miami homes.

Wind Mitigation Inspection Features

The Florida Office of Insurance Regulation Form OIR-B1-1802 evaluates specific features.

Feature 1: Roof Covering

What It Evaluates : Roof material type and installation method

Discount Potential : Up to 15%

Rating Categories :

- FBC (Florida Building Code) Approved: Materials meeting current code standards

- Non-FBC: Older materials not meeting current standards

- Concrete/Clay tile: Premium materials with excellent wind resistance

- Metal: Standing seam or metal shingles designed for high winds

- Architectural shingles: Modern wind-resistant shingles

Inspection Process :

- Verify roofing material type

- Check installation date (building permit or records)

- Confirm compliance with building codes in effect at installation

- Document with photos

How to Qualify :

- New roof installed to current Florida Building Code

- Roof replacement with code-compliant materials

- Documentation of existing code-compliant roof

- Impact-resistant shingles provide additional benefits

Feature 2: Roof Deck Attachment

What It Evaluates : How roof sheathing attaches to roof structure

Discount Potential : Up to 21%

Rating Categories :

- A: Standard 8d nails, 6"/12": Basic attachment (minimal discount)

- B: Staples: Weakest attachment (no discount)

- C: Enhanced nailing (8d every 6"): Better than standard

- D: Superior nailing (8d ring shank every 6"): Best attachment method

Inspection Process :

- Access attic to view underside of roof deck

- Examine fastener type and spacing

- Document attachment method

- Verify throughout multiple roof areas

How to Qualify :

- Homes built after 2002 typically have enhanced nailing (Miami-Dade requirements)

- Older homes may need re-roofing to upgrade attachment

- Can sometimes upgrade during roof replacement

Challenge : Attic access required. Inspectors cannot verify without seeing underside of roof deck.

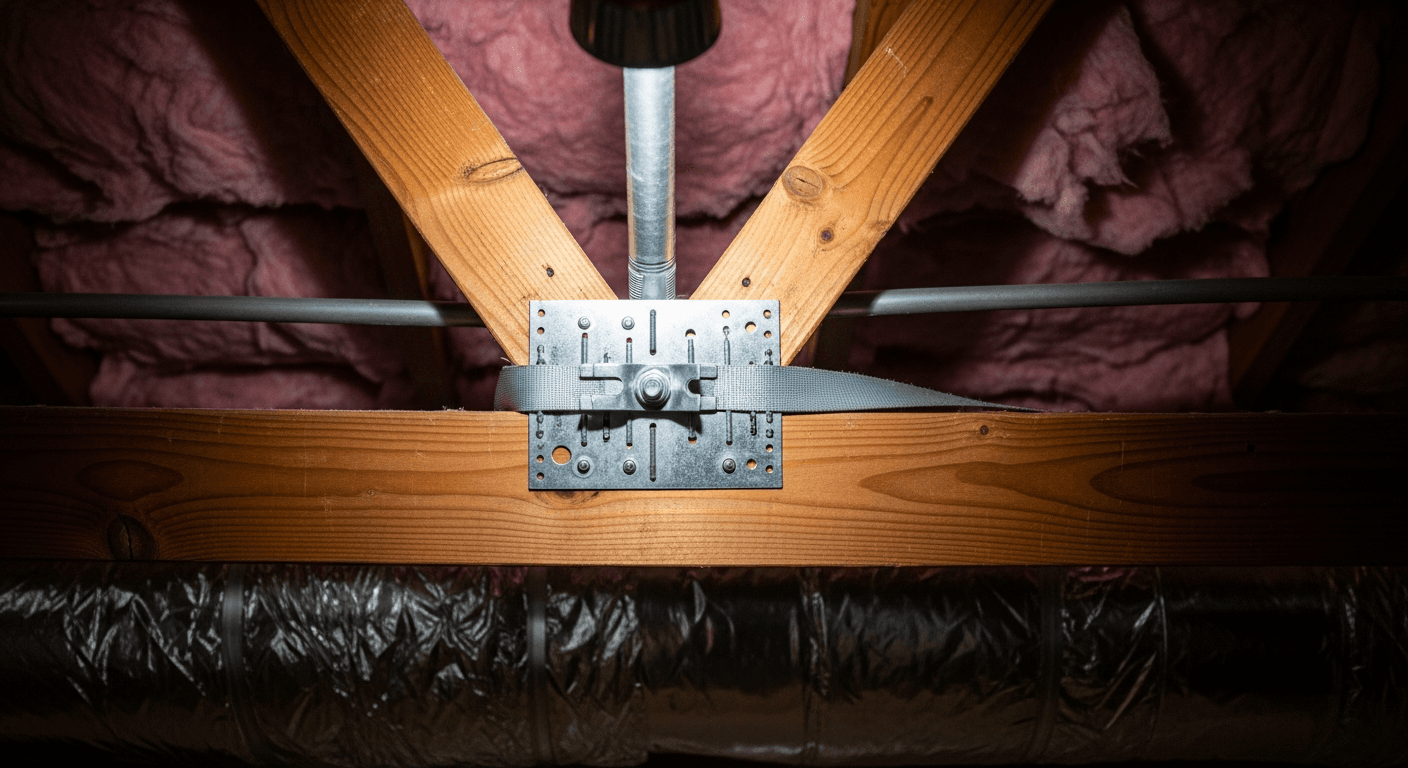

Feature 3: Roof-to-Wall Attachment

What It Evaluates : How roof structure connects to walls

Discount Potential : Up to 32% (largest single discount)

Rating Categories :

- Toe nails: Basic connection (minimal discount)

- Clips: Metal connectors between trusses/rafters and walls

- Single wraps: Metal straps wrapping over truss/rafter

- Double wraps: Straps wrapping both sides of truss/rafter

Inspection Process :

- Access attic to view truss-to-wall connections

- Identify hurricane straps, clips, or wraps

- Document connection method with photos

- Verify connections throughout structure

How to Qualify :

- Homes built after 2001 in Miami-Dade typically have hurricane straps

- Older homes may have clips (common in 1990s construction)

- Older homes with only toe nails receive minimal/no discount

- Retrofit installation possible but expensive ($2,000-$8,000 depending on home)

Feature 4: Opening Protection

What It Evaluates : Protection for windows, doors, and garage doors

Discount Potential : Up to 41% (when combined with other features)

Rating Categories :

- None: No hurricane protection

- Basic: Some openings protected

- Hurricane: Impact-resistant windows/doors OR hurricane shutters for all openings

- Other: Garage door reinforcement, etc.

Protection Types :

Impact-Resistant Windows and Doors :

- Laminated glass that resists penetration

- Expensive ($500-$1,200 per window)

- Permanent solution

- Aesthetic benefits

- Highest insurance discounts

Hurricane Shutters :

- Accordion shutters: Permanent install, deploy quickly

- Roll-down shutters: Premium option, remote operated

- Panel shutters: Removable, storage required, lower cost

- Colonial shutters: Aesthetic permanent option

- Bahama shutters: Decorative and functional

Garage Door Reinforcement :

- Bracing systems for standard garage doors

- Retrofit reinforcement kits ($200-$800)

- Wind-rated garage doors (if replacing)

Inspection Process :

- Document all window and door protection

- Verify impact ratings on windows/doors

- Photograph protection systems

- Confirm compliance with required wind ratings

How to Qualify :

- Install impact windows/doors (most expensive, highest discount)

- Install hurricane shutters (moderate cost, good discount)

- Reinforce garage door (lowest cost upgrade)

- Even partial protection provides some discount

Feature 5: Secondary Water Resistance (SWR)

What It Evaluates : Protection if roof covering fails

Discount Potential : Up to 3% (smaller discount but easy to obtain)

Rating Categories :

- Yes: Sealed roof deck (underlayment covering entire roof)

- No: Traditional felt paper only at certain areas

Protection Types :

- Self-adhering polymer modified bitumen (ice and water shield)

- Peel-and-stick rubberized underlayment

- Must cover entire roof deck, not just eaves and valleys

How to Qualify :

- Install during roof replacement

- Relatively inexpensive upgrade ($500-$1,500 additional on re-roof)

- Most new Florida roofs include this automatically

- Older roofs unlikely to qualify unless recently replaced

Feature 6: Roof Geometry

What It Evaluates : Roof shape and configuration

Discount Potential : Small discount (exact amount varies by insurer)

Rating Categories :

- Hip roof: All sides slope down (best for wind resistance)

- Gable roof: Two sides slope, two sides vertical

- Flat roof: Minimal slope

- Other: Complex configurations

Why It Matters :

- Hip roofs resist wind uplift better than gable roofs

- Gable ends are vulnerable to wind pressure

- Cannot change without major reconstruction

- Discount applies to existing geometry (no upgrade possible)

Inspection Process :

- Visual assessment from exterior

- Roof shape documentation

- Gable end bracing evaluation (if applicable)

The Inspection Process

Understanding what happens during wind mitigation inspection helps preparation and expectations.

Scheduling Your Inspection

When to Schedule :

- After any roof work (immediately)

- When purchasing a home (before insurance binds)

- Every few years to update form (some features improve over time)

- After hurricane retrofitting work

Who Performs Inspections :

Licensed professionals authorized to complete OIR-B1-1802 forms:

- Licensed roofers (General or Roofing Contractor license)

- Licensed home inspectors

- Licensed engineers

- Some insurance agents (if properly licensed)

Cost : $75-$150 typically (often combined with 4-point inspection for $200-$250 total)

Duration : 30-45 minutes on-site

What Happens During Inspection

Exterior Evaluation :

- Overall roof condition assessment

- Roof covering material identification

- Roof geometry documentation

- Opening protection verification

- Photo documentation of all features

Interior/Attic Evaluation :

- Attic access for deck attachment examination

- Truss-to-wall connection evaluation

- Structural assessment

- Photo documentation of connections

Documentation Review :

- Building permits (if available)

- Previous inspection reports

- Roof installation receipts

- Window/door specifications

Form Completion :

- Inspector completes OIR-B1-1802 form

- Signs and seals document

- Provides copy to homeowner

- May submit directly to insurance company

Required Access

For Complete Inspection :

- Roof access (inspector will access safely)

- Attic access (essential for deck and wall connection ratings)

- Garage access (for door evaluation)

- Window and door specifications or purchase receipts

Attic Access Critical : Without attic access, inspector cannot verify roof deck attachment or roof-to-wall connections. losing substantial discount potential.

Preparation :

- Clear attic access hatch

- Remove stored items blocking access

- Ensure lighting available

- Have any documentation ready

After the Inspection

Receive OIR-B1-1802 Form :

- Completed and signed by licensed inspector

- Includes ratings for all evaluated features

- Photo documentation attached

- Valid for 5 years (7 years if no opening protection claimed)

Submit to Insurance Company :

- Provide form with next insurance renewal

- If new construction or major improvements, submit immediately

- Some inspectors submit directly (confirm this service)

- Keep copy for your records

Expect Premium Reduction :

- Discounts applied at next renewal or policy change

- Can take one billing cycle to appear

- Review policy carefully to confirm all applicable discounts

- Contact insurer if discounts missing

Maximizing Your Discounts

Strategic improvements provide best return on investment.

Low-Cost Improvements with High Returns

Priority 1: Roof Deck Attachment (If Re-roofing)

When replacing roof, ensure proper nailing specification:

- 8d ring shank nails every 6" provides maximum rating

- Minimal additional cost during roof replacement ($200-$500)

- Cannot upgrade without full roof replacement

- Discount: Up to 21% premium reduction

- ROI: Pays for upgrade in first year typically

Priority 2: Secondary Water Resistance (During Re-roof)

Install peel-and-stick underlayment on entire roof deck:

- Adds $500-$1,500 to roof replacement cost

- Easy upgrade during any roof work

- Provides actual storm protection benefit

- Discount: Up to 3% premium reduction

- ROI: 2-3 years typically

Priority 3: Garage Door Reinforcement

Install bracing kit for existing garage door:

- Cost: $200-$800 for DIY or professional installation

- Improves opening protection rating

- Actual wind resistance benefit

- Discount: Partial opening protection credit (5-10% potential)

- ROI: 1-2 years typically

Explore roof replacement options that maximize wind mitigation benefits.

Moderate-Cost Improvements

Priority 4: Hurricane Shutters

Install accordion or roll-down shutters:

- Cost: $2,000-$10,000 depending on home size and type

- Provides full opening protection credit

- Actual storm protection for windows

- Discount: Up to 41% when combined with other features (often 20-30% incremental)

- ROI: 3-7 years typically

- Secondary benefit: Property protection during storms

Priority 5: Impact-Resistant Windows (When Replacing)

When replacing windows anyway, upgrade to impact-resistant:

- Premium over standard: $200-$500 per window

- Permanent solution with aesthetic benefits

- Highest opening protection credit

- Energy efficiency improvements

- Discount: Same as shutters (20-30% typical)

- ROI: 5-10 years on insurance alone, better with energy savings

High-Cost Improvements (Usually Not Cost-Justified)

Roof-to-Wall Connection Retrofit :

- Cost: $2,000-$8,000 for whole-house installation

- Significant discount potential (up to 32%)

- Problem: High labor cost, requires extensive attic work

- ROI: Often 10-20 years on insurance savings alone

- Better Strategy: Negotiate with current straps/clips, wait for other major work

Complete Impact Window Replacement :

- Cost: $15,000-$50,000 depending on home size

- Highest opening protection rating

- Problem: Very expensive for insurance savings alone

- ROI: 15-30 years on insurance savings

- Better Strategy: Only if replacing windows anyway or valuing storm protection highly

Insurance Discount Details

Understanding discount structure helps set realistic expectations.

Discount Ranges by Feature

Based on Florida law and typical insurer rates:

| Feature | Potential Discount | Typical Home Savings |

|---|---|---|

| Roof Covering (FBC) | Up to 15% | $150-$300/year |

| Roof Deck Attachment (Superior) | Up to 21% | $200-$400/year |

| Roof-to-Wall (Clips/Straps) | Up to 32% | $300-$600/year |

| Opening Protection (Full) | Up to 41%* | $400-$800/year |

| Secondary Water Resistance | Up to 3% | $30-$60/year |

| Hip Roof | Varies | $50-$150/year |

*Opening protection discount is not additive with others. it interacts with roof features for combined maximum discount around 45%.

How Discounts Combine

Not Simply Additive : Discounts interact in complex ways specified by insurance rate filings. Maximum combined discount typically 40-50%, not cumulative of all individual discounts.

Example Scenario :

Miami single-family home, $250,000 coverage, base premium $2,500/year:

- FBC roof covering: -12% ($300 savings)

- Superior roof deck attachment: -18% ($450 savings)

- Hurricane straps (clips): -28% ($700 savings)

- Hurricane shutters: -38% ($950 savings)

- Total combined discount: ~42% ($1,050 savings)

Reality : Discounts overlap and reduce each other's impact, so final combined discount less than sum of parts.

Variability by Insurer

Different Insurers, Different Discounts :

- Some carriers weight certain features more heavily

- Citizens Property Insurance often provides lowest discounts

- Private carriers may offer better wind mitigation recognition

- Shopping insurance with completed wind mit form provides better rates

Remarket After Improvements :

- Complete wind mitigation improvements

- Get updated wind mit form

- Shop multiple insurance carriers

- Often find 20-40% lower premiums from carrier recognizing improvements

Common Scenarios and Recommendations

Scenario 1: Home Built Pre-1994

Typical Features :

- Older roof (likely needs replacement)

- Toe nail roof-to-wall connections only

- Standard nailing (A rating)

- No opening protection

- Traditional felt underlayment

Recommendations :

1. When replacing roof:

- Specify superior nailing (8d ring shank every 6")

- Install SWR underlayment across entire deck

- Use FBC-compliant roofing materials

- Cost: $15,000-$25,000

- Insurance Impact: 25-35% discount typical

2. Add garage door bracing:

- - Cost: $400-$800

- - Insurance Impact: Additional 5-10%

3. Consider hurricane shutters (longer-term):

- - Cost: $3,000-$8,000

- - Insurance Impact: Additional 10-20%

Estimated Total Savings : $600-$1,200 annually on insurance

Scenario 2: Home Built 2002-Present

Typical Features :

- Enhanced or superior nailing (C or D rating)

- Hurricane straps or clips (single or double wraps)

- FBC-compliant roof (if original or recently replaced)

- May have some opening protection

- Possibly SWR if built post-2007

Recommendations :

1. Get wind mitigation inspection immediately (if not done):

- Cost: $100-$150

- Insurance Impact: 30-40% discount typical for homes with existing features

- Savings: $500-$900 annually

2. Add opening protection if missing:

- - Garage door bracing: $400-$800

- - Consider accordion shutters for windows

- - Insurance Impact: Additional 10-15%

3. Ensure SWR if re-roofing:

- - Minimal additional cost

- - Confirms discount eligibility

Estimated Total Savings : $700-$1,000+ annually

Scenario 3: Recently Purchased Home

Action Plan :

1. Schedule inspection within 30 days of closing:

- Provides baseline of existing features

- Identifies improvement opportunities

- Allows insurance shopping with accurate form

2. Submit form to insurance company immediately:

- - Many buyers overpay first year due to missing wind mit form

- - Discounts often apply retroactively within policy period

3. Plan improvements for next 1-2 years:

- - Prioritize based on ROI analysis

- - Coordinate with any planned renovations

Wind Mitigation Inspection Providers

Selecting an Inspector

Qualifications to Verify :

- Florida contractor or home inspector license

- Experience completing OIR-B1-1802 forms

- Professional liability insurance

- Local market knowledge

- Photo documentation provided

- Direct insurance company submission available

Questions to Ask :

1. What's your license number and type?

2. How many wind mitigation inspections have you completed?

3. What does inspection include?

4. Will you access attic and roof?

5. When will I receive completed form?

6. Do you submit directly to insurance companies?

7. What if I disagree with ratings?

Red Flags :

- Guaranteeing specific ratings before inspection

- Unwilling to access attic or roof

- Rushing through inspection (under 20 minutes)

- No photo documentation

- Incomplete form sections

- Unlicensed operators

Costs and Bundling

Standalone Wind Mitigation : $75-$150

Combined with 4-Point Inspection : $200-$300 total (better value)

- 4-point inspection required by many insurers anyway

- Evaluates roof, electrical, plumbing, HVAC

- Same inspector, same visit, better pricing

Combined with Home Inspection (home purchase): $400-$600 total

- Includes complete home inspection plus wind mit

- Ideal timing for new homeowners

- Most comprehensive assessment

Extreme Roofing Wind Mitigation Services :

As licensed roofing contractor, we provide wind mitigation inspections separately or combined with roofing services. When performing roof replacement, wind mitigation inspection included to document your new improvements.

Conclusion: Wind Mitigation Pays for Itself

Wind mitigation inspections are among the highest-ROI investments Miami homeowners can make. For $75-$150, most homeowners save $300-$1,200 annually on insurance premiums. paying for inspection in first year and continuing savings for years ahead.

Even without making improvements, documenting existing wind-resistant features through professional inspection often reveals discounts homeowners didn't know they qualified for. Combined with strategic improvements during normal home maintenance (like roof replacement), wind mitigation provides both insurance savings and real storm protection.

Key Takeaways for Miami Homeowners :

- Schedule wind mitigation inspection to document existing features

- Complete form saves $300-$1,200 annually for most homes

- Maximize discounts during roof replacement with proper specifications

- Opening protection (shutters or impact windows) provides substantial savings

- Shop insurance with completed form for best rates

- Form valid 5-7 years. update after any improvements

- ROI typically under 2 years for most improvements

Ready to maximize your insurance savings? Extreme Roofing Inc. provides certified wind mitigation inspections and roofing services that qualify for maximum discounts. Whether you need standalone inspection or are planning roof replacement, we document all eligible features and explain improvement options.

Call 305-225-1535 or request your wind mitigation inspection today. We'll thoroughly evaluate your home, complete official OIR-B1-1802 form, provide detailed photo documentation, explain your ratings and potential improvements, and submit directly to your insurance company. Since 2004, we've helped thousands of Miami homeowners reduce insurance costs through proper wind mitigation documentation.

Learn about 4-point inspections | Explore roof replacement | Hurricane preparation guide

Frequently Asked Questions

How much can I save with wind mitigation inspection in Miami?

Miami homeowners typically save $300-$1,200 annually on homeowners insurance with completed wind mitigation inspection documenting qualifying features. Homes with superior roof deck attachment, hurricane straps, impact windows or shutters, and FBC-compliant roofs can receive 40-50% premium discounts. Average Miami home paying $2,500/year for insurance saves $1,000/year with full wind mitigation features documented. Inspection costs $75-$150, paying for itself in first few months through insurance savings. Savings continue annually for life of features (5-7 years minimum between inspections). Specific savings depend on current premium, carrier, and qualifying features.

What does a Miami wind mitigation inspection include?

Miami wind mitigation inspection evaluates six key features on official OIR-B1-1802 form: roof covering type and installation method (15% discount potential), roof deck attachment method (21% discount), roof-to-wall connections (32% discount), opening protection for windows/doors (41% combined discount), secondary water resistance, and roof geometry. Inspector accesses roof and attic to document features with photos, completes official form, and provides documentation for insurance submission. Inspection takes 30-45 minutes, costs $75-$150, and results valid 5-7 years. Attic access essential for maximum ratings. without it, inspector cannot verify critical deck and wall connections.

When should I get a wind mitigation inspection in Miami?

Schedule Miami wind mitigation inspection: immediately after roof replacement (document new qualifying features), when buying home (reduces insurance costs from day one), after installing hurricane shutters or impact windows, every 5-7 years to update form, or anytime you haven't had one before (may have qualifying features you're not getting credit for). New homeowners should get inspection within 30 days of closing. many overpay first year without wind mit form. After any home improvements affecting wind resistance, update inspection to capture additional discounts. Even older homes often have some qualifying features worth documenting.

Do I need wind mitigation inspection for home insurance in Florida?

Wind mitigation inspection isn't legally required for Florida home insurance, but it's practically essential for Miami homeowners. Without completed OIR-B1-1802 form, insurance companies assume your home lacks wind-resistant features and charge maximum premiums. Florida law requires insurers to offer discounts for qualifying features. but you must prove features exist through certified inspection. Cost of NOT having inspection: $300-$1,200 annually in foregone insurance savings. Most Miami lenders and insurance agents strongly recommend wind mitigation inspection because premium savings typically exceed inspection cost within 2-3 months. Only reason to skip: rental property with no insurance, or home being demolished soon.

How long is wind mitigation inspection valid in Miami?

Miami wind mitigation inspections remain valid 5 years if claiming opening protection discounts (hurricane shutters or impact windows) or 7 years if not claiming opening protection. Validity period begins from inspection date on OIR-B1-1802 form. However, get new inspection sooner if you make improvements affecting wind resistance: roof replacement, hurricane shutter installation, impact window installation, or structural retrofits. New inspection documents improvements and updates discounts immediately rather than waiting for expiration. Insurance companies accept valid forms from any approved inspector. you don't need re-inspection when switching carriers if current form still valid. Keep copies of all wind mitigation forms. they're valuable documents worth hundreds annually.

Need Roofing Help?

Whether you need an inspection, repair, or full replacement, our team of licensed roofing professionals is ready to help. Serving South Florida since 2004.

Related Articles

Everything Miami homeowners need to know about four-point inspections. what's evaluated, costs, when you need one, and how to prepare for this critical insurance requirement.

Read More

Florida insurance rates are dropping for the first time since 2015. Learn how combining market rate decreases with strategic roof upgrades can save Miami homeowners $1,400-$2,600 per year on premiums.

Read More

Everything Miami homeowners need to know about professional roof inspections . what inspectors check, how much it costs, how often you need one, and how inspections save you thousands in preventable damage.

Read More