Florida Insurance Rates Are Finally Dropping in 2026: How Your Roof Can Save You Even More

Florida Insurance Rates Are Finally Dropping. Here's How to Stack the Savings.

For the first time since 2015, Florida insurance rates are moving in the right direction. Citizens Property Insurance, the state-backed insurer of last resort, just approved its first rate decrease in over a decade, with Miami-Dade getting an average 14.0 percent cut and Broward getting 14.1 percent. That's real money back in every homeowner's pocket, and it represents the first concrete payoff from the insurance reforms that started in 2022.

But the rate decrease is only half the story. Homeowners who combine the 2026 rate cut with strategic roof upgrades can stack the savings and turn a good year into a transformative one. Here's the math: a Miami-Dade homeowner paying $6,000 per year in premiums saves $834 from the Citizens rate cut. Add a new roof with proper wind mitigation credits, and that same homeowner saves another $600 to $1,800 per year on top. Total annual savings: $1,400 to $2,600.

I've been helping Miami homeowners capture these insurance savings for over 20 years, and 2026 is the best window I've seen for this strategy. Here's exactly how to combine the rate decrease with roof upgrades, what to do first, and which Miami neighborhoods see the biggest total savings.

This guide breaks down every element of the 2026 insurance landscape, explains exactly how roof improvements multiply your savings, and provides actionable steps to maximize every dollar of premium reduction available to you.

The 2026 Rate Decrease: What Is Actually Happening

The Florida insurance market has been in crisis since 2017. A combination of catastrophic hurricane losses, rampant litigation abuse, and insurer insolvencies pushed premiums to the highest levels in the nation. By 2023, the average Florida homeowner paid $4,231 annually for property insurance, roughly triple the national average. Some homeowners in coastal South Florida were paying $8,000 to $15,000 per year, and many found it impossible to obtain coverage from any private carrier at all.

That trajectory has finally reversed. The reforms that began in late 2022 have taken root, and the data is clear: the market is turning. Here is what changed and what the numbers look like across South Florida.

Citizens Property Insurance Rate Changes by County

Citizens Property Insurance is the benchmark that private carriers follow. As the state-backed insurer of last resort, Citizens sets the floor for the market. When Citizens rates drop, private market rates typically follow within 6 to 12 months as carriers compete to attract policyholders away from Citizens.

| County | Average Rate Decrease | Estimated Annual Savings (on $4,500 policy) | Effective Date |

|---|---|---|---|

| Miami-Dade | 14.0% | $630 | January 2026 |

| Broward | 14.1% | $635 | January 2026 |

| Palm Beach | 12.8% | $576 | January 2026 |

| Monroe (Keys) | 11.2% | $504 | January 2026 |

| Hillsborough (Tampa) | 13.5% | $608 | January 2026 |

| Duval (Jacksonville) | 10.9% | $491 | January 2026 |

| Lee (Fort Myers) | 15.3% | $689 | January 2026 |

| Pinellas (St. Pete) | 13.8% | $621 | January 2026 |

| Orange (Orlando) | 12.1% | $545 | January 2026 |

| Statewide Average | 13.2% | $594 | January 2026 |

These are Citizens-specific reductions. Private market carriers are independently filing rate decreases ranging from 5% to 18%, depending on the company and region. The overall trend is unmistakable: rates are coming down across the board for the first time in nearly a decade.

Why Rates Are Dropping Now

The rate decrease did not happen by accident. It is the result of specific legislative reforms that fundamentally changed the Florida insurance ecosystem. Understanding these reforms helps homeowners appreciate that this is a structural shift, not a temporary blip:

- SB 2-D (December 2022): Eliminated one-way attorney fee provisions in insurance litigation, which was the single largest driver of inflated claims. Florida accounted for 8% of homeowner insurance claims nationally but 76% of all homeowner insurance lawsuits. The one-way fee structure incentivized attorneys to file suit on virtually every denied or underpaid claim, driving up costs for every policyholder in the state

- SB 7052 (2023): Created the Reinsurance to Assist Policyholders (RAP) program, reducing reinsurance costs for carriers by providing a state-backed layer of catastrophic coverage. This saved the industry an estimated $1 billion in annual reinsurance costs, savings that are now flowing through to policyholders

- HB 799 (2024): Strengthened fraud prosecution and accelerated claims resolution timelines. The law created new criminal penalties for organized insurance fraud rings and required insurers to make initial claim decisions within 60 days

- 17 new carriers: Since the 2022 reforms, 17 new insurance companies have entered or re-entered the Florida market, dramatically increasing competition. Companies like Slide Insurance, TypTap, Safepoint, and Heritage have aggressively priced policies to gain market share

- Citizens depopulation: Citizens policy count dropped 73% from its peak of approximately 1.4 million policies to roughly 385,000 as of February 2026, as private carriers absorbed risk. This depopulation is the clearest signal that the private market views Florida as viable again

- Reduced litigation: Insurance litigation filings in Florida dropped 58% between 2023 and 2025, according to the Florida Office of Insurance Regulation. This reduction in legal costs is the primary driver of the rate decreases homeowners are now seeing

The combination of reduced litigation costs, increased competition, expanded reinsurance capacity, and aggressive carrier entry has created the conditions for meaningful premium relief for the first time in a decade.

How Your Roof Directly Affects Your Insurance Premium

Insurance companies price your policy based on risk. Your roof is the single largest factor in that risk calculation because it is the primary barrier between a hurricane and the interior of your home. The condition, age, material, and wind-resistance features of your roof determine a significant portion of your premium, often 30-40% of the total cost.

Understanding this relationship is essential to maximizing your savings in 2026, because the market rate decrease and the roof-based discount are independent of each other. They are calculated separately and applied separately. You can stack both.

The Five Roof Factors Insurers Evaluate

Every Florida insurance company evaluates these five factors when calculating the roof-related portion of your premium:

- Roof age: Newer roofs receive dramatically better rates. Florida insurers heavily penalize roofs older than 15 years, and many refuse to write new policies on roofs older than 20 years. A 5-year-old roof can save you 15-25% compared to a 20-year-old roof of the same material, all else being equal

- Roof material: Impact-resistant and wind-rated materials like standing seam metal, concrete tile, and Class 4 architectural shingles with high wind ratings earn significant discounts. The material type determines how your roof performs in the wind speed categories that define Florida hurricane risk

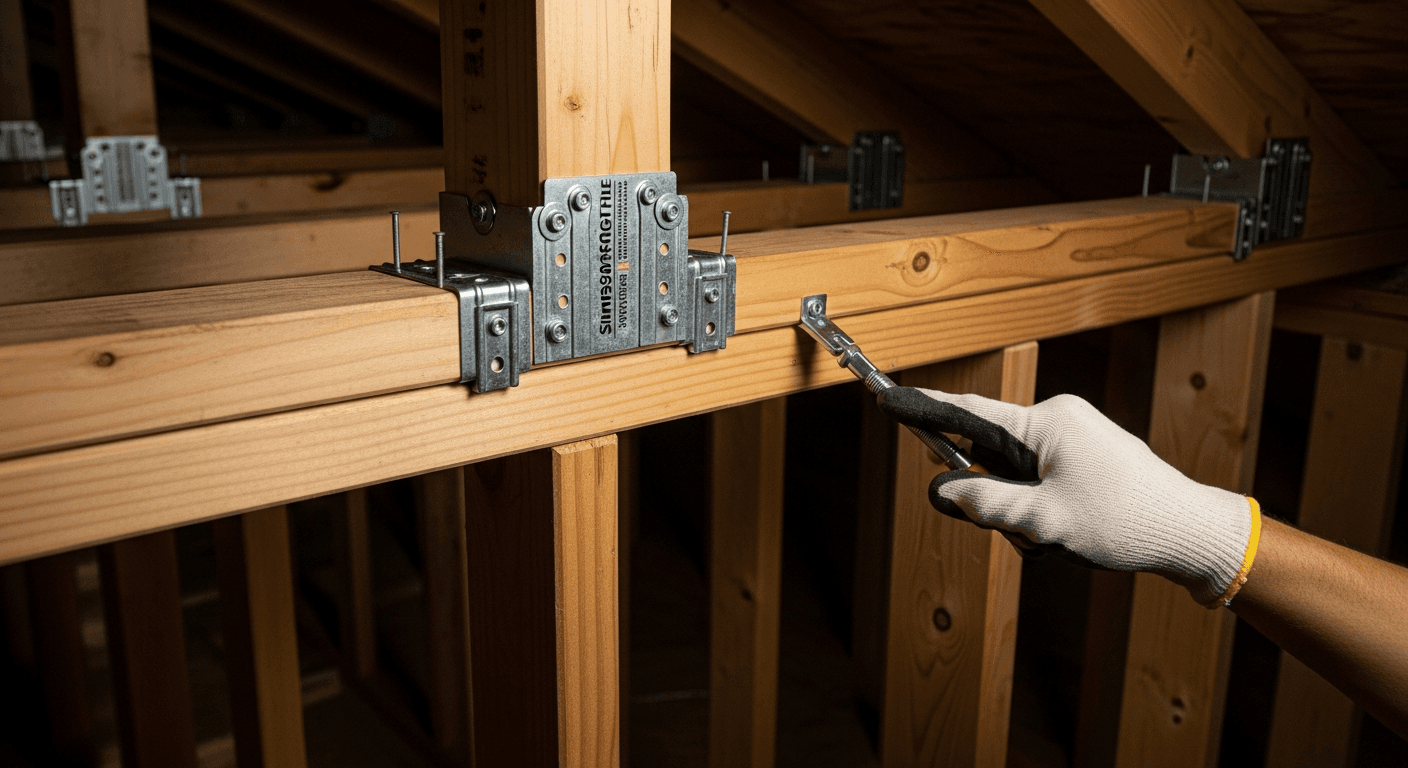

- Roof-to-wall connections: Hurricane straps and clips that anchor the roof structure to the walls are among the single most important factors in wind mitigation. These connections prevent the roof from lifting off during high winds, and the type of connection (toe-nail, clip, single wrap, double wrap) directly determines your discount level, ranging from 10-30% of your premium

- Roof deck attachment: The method used to fasten roof sheathing (plywood or OSB) to the trusses affects your rating significantly. Standard 6d nails provide minimal protection. Ring-shank 8d nails at 6-inch spacing earn the highest rating and the largest discount. This is evaluated as Section 2 on the wind mitigation form

- Secondary water barrier (SWB): A self-adhering modified bitumen membrane applied over the entire roof deck provides backup waterproofing if shingles or tiles are lost during a storm. This feature earns a substantial discount because it dramatically reduces the severity of claims when roof covering is lost, which is the most common form of hurricane roof damage

How Different Roof Types Stack Savings on Top of the 2026 Market Decrease

This is where the math gets compelling. The 2026 market rate decrease applies to your base premium regardless of your roof. But a roof upgrade earns you an additional, independent discount on top of that reduced base. The savings multiply rather than simply add.

| Roof Improvement | Additional Premium Reduction | Annual Savings on $6,000 Policy | Combined with 14% Market Drop |

|---|---|---|---|

| Standing seam metal roof | 15-25% | $900-$1,500 | $1,740-$2,340 |

| Concrete tile (new, FBC compliant) | 10-18% | $600-$1,080 | $1,440-$1,920 |

| Architectural shingles (Class 4 impact) | 8-15% | $480-$900 | $1,320-$1,740 |

| Hurricane straps + clips upgrade | 10-30% | $600-$1,800 | $1,440-$2,640 |

| Secondary water barrier (full deck) | 5-10% | $300-$600 | $1,140-$1,440 |

| Full wind mitigation package | 20-45% | $1,200-$2,700 | $2,040-$3,540 |

Note: Percentages vary by insurer and policy. Actual savings depend on your current premium, coverage amounts, deductible levels, and specific policy provisions. The figures above represent documented ranges from major Florida carriers including Citizens, Universal, Heritage, Slide, and TypTap.

Why Standing Seam Metal Roofs Earn the Largest Discounts

Standing seam metal roofs consistently earn the highest insurance discounts among all roofing materials for several reasons that directly translate to lower insurer risk:

- Wind resistance: Standing seam metal panels interlock along raised seams, creating a continuous surface with no exposed fasteners. This design withstands winds exceeding 180 mph when properly installed, well above the Category 5 threshold

- Impact resistance: Metal roofing resists impact from flying debris that would crack tiles or tear shingles. This reduces the frequency and severity of wind-related claims

- Non-combustible: Metal roofs do not catch fire from lightning strikes or airborne embers, eliminating an entire category of claim risk

- Longevity: A properly installed standing seam metal roof lasts 40 to 70 years, meaning the insurer is covering a roof material that will not deteriorate and require replacement during the policy term

- Class 4 hail rating: Most standing seam metal products carry the highest hail resistance classification, which earns premium credits in areas subject to convective storm damage

The combination of these performance characteristics is why insurers reward metal roofing with the largest available discounts. For homeowners who are considering a roof replacement, the insurance savings alone can justify the premium cost of metal over conventional shingles.

The "Double Savings" Strategy: Market Drop + Roof Upgrade

The most financially savvy approach for 2026 is what we call the "double savings" strategy. Instead of passively accepting the market rate decrease and doing nothing else, you proactively invest in roof improvements that earn additional premium reductions, effectively compounding your savings.

Combined Savings Projection for a Typical Miami-Dade Homeowner

Consider a homeowner in Miami-Dade County currently paying $6,000 per year in property insurance premiums on a home with a 17-year-old shingle roof and no documented wind mitigation features. Here is how the savings stack when they take action:

| Savings Source | Calculation | Annual Savings |

|---|---|---|

| Citizens rate decrease (14%) | $6,000 x 0.14 | $840 |

| New standing seam metal roof (20% additional) | $5,160 x 0.20 | $1,032 |

| Wind mitigation credits (additional 10%) | $4,128 x 0.10 | $413 |

| Shopping competing carriers (conservative) | 5% additional | $186 |

| Total combined annual savings | $2,471 | |

| New annual premium | $3,529 |

That is a 41% reduction in annual insurance costs. Over 10 years, assuming modest rate increases in future years, this homeowner saves approximately $20,000 to $25,000 in cumulative premium reductions. Over 20 years, the savings approach $40,000 to $50,000.

The Passive Homeowner vs. the Proactive Homeowner

To illustrate the long-term impact, compare two identical Miami-Dade homeowners both paying $6,000 per year in 2025:

Passive homeowner : Does nothing. Receives the 14% market decrease passively. New premium: $5,160. Saves $840 per year. Over 10 years: approximately $8,400 in total savings.

Proactive homeowner : Invests in a new metal roof with full wind mitigation. New premium: $3,529. Saves $2,471 per year. Over 10 years: approximately $24,710 in total savings, minus the out-of-pocket roof investment.

The proactive homeowner saves nearly three times more than the passive homeowner, and the gap widens every year as premiums compound.

Payback Period on a Roof Investment

A new standing seam metal roof for a typical Miami-Dade home costs $18,000 to $35,000 depending on the size and complexity. If the homeowner accesses the My Safe Florida Home grant (up to $10,000), the out-of-pocket cost drops to $8,000 to $25,000. With combined annual insurance savings of $1,400 to $2,600, the insurance payback period alone is 3 to 12 years.

Factor in the additional financial benefits and the picture becomes even more compelling:

- Increased home value: A metal roof adds $15,000 to $40,000 in resale value depending on the property and market

- Energy savings: Reflective metal roofing reduces cooling costs by $300 to $800 per year in South Florida's climate

- Extended lifespan: Metal roofs last 40-70 years vs. 15-20 years for shingles, eliminating at least one to two additional roof replacements over the life of the home

- Reduced maintenance: Metal roofs require virtually no maintenance compared to the periodic repairs that shingle and tile roofs demand

A complete re-roofing with wind mitigation features installed is one of the highest-ROI home improvements available to Florida homeowners in 2026.

Timeline of Florida Insurance Reforms (2022-2026)

Understanding how we arrived at this moment helps homeowners appreciate the stability of the current trajectory. These reforms are structural changes to the legal and regulatory framework, not temporary market conditions, which means the rate relief is likely to persist and potentially accelerate.

| Date | Reform | Impact |

|---|---|---|

| December 2022 | SB 2-D: Tort reform eliminates one-way attorney fees | Reduced litigation costs by an estimated 40-60% over two years. Lawsuit filings dropped 58% |

| March 2023 | SB 7052: RAP reinsurance program created | Reduced carrier reinsurance costs by $1 billion statewide annually |

| June 2023 | Citizens surcharge eliminated for new policyholders | Reduced barriers for Citizens policyholders to shop private market alternatives |

| January 2024 | HB 799: Fraud prosecution strengthened | Reduced fraudulent claims filing by an estimated 25%. Created new criminal penalties |

| July 2024 | 12 new carriers enter Florida market | Increased competition drove private market rates down 3-8% in most counties |

| January 2025 | My Safe Florida Home program funded ($280 million) | Homeowner grants up to $10,000 for roof hardening improvements. 2:1 state match |

| October 2025 | 5 additional carriers enter Florida market | Total of 17 new carriers since reform, further increasing competition for policyholders |

| January 2026 | Citizens approves first rate decrease since 2015 | Miami-Dade 14.0%, Broward 14.1%, statewide average 13.2% |

| July 1, 2026 | HB 815: Roof age loophole closed | Insurers cannot non-renew solely for roof age if 5+ years remaining useful life certified |

What HB 815 Means for Homeowners (Effective July 1, 2026)

HB 815 is a particularly important piece of legislation that many homeowners have not yet heard about. Starting July 1, 2026, insurance companies can no longer refuse to write or renew a policy solely because of the age of the roof, provided a licensed inspector certifies that the roof has at least five years of remaining useful life.

This closes a loophole that insurers had been exploiting aggressively since 2020, where they would non-renew policies on homes with roofs older than 15 years regardless of the roof's actual condition. Tens of thousands of Florida homeowners received non-renewal notices between 2020 and 2025 based solely on roof age, forcing them into expensive emergency roof replacements or relegating them to Citizens at higher premiums. Under HB 815:

- Insurers must accept a licensed inspection showing 5+ years of remaining useful life as sufficient documentation

- Non-renewal notices based solely on roof age are prohibited if the inspection passes the 5-year remaining life threshold

- Homeowners can challenge any non-renewal with documentation from a licensed roofing contractor, licensed building inspector, or licensed general contractor

- Carriers face penalties under the Florida Insurance Code for systematic non-renewals that violate the statute

- The inspection must be performed within 12 months preceding the insurer's coverage decision

This means homeowners with well-maintained older roofs have significantly more leverage and protection starting in mid-2026. However, homeowners with genuinely deteriorating roofs should still prioritize replacement, as the inspection must be honest and the 5-year remaining life threshold is a real standard that inspectors must certify in good faith.

For homeowners who want to understand the full relationship between roof age and insurance, read our complete guide on the 15-year roof rule in Florida.

Wind Mitigation: The Biggest Insurance Discount Most Homeowners Miss

A wind mitigation inspection is a standardized evaluation of your home's hurricane-resistant features using the Florida Office of Insurance Regulation Form OIR-B1-1802. Florida law requires insurance companies to offer discounts for homes that pass specific wind mitigation criteria, but the homeowner must initiate the inspection and submit the results. The insurer will not proactively give you a discount you have not documented.

The average savings from a complete wind mitigation inspection is $981 per year, according to data from the My Safe Florida Home program. Yet a staggering number of Florida homeowners have never had a wind mitigation inspection performed, leaving hundreds to thousands of dollars in annual savings unclaimed. Industry estimates suggest that 40-50% of eligible Florida homeowners do not have a current wind mitigation report on file with their insurer.

What a Wind Mitigation Inspection Evaluates

The inspection covers seven specific areas documented on the OIR-B1-1802 form, each of which can contribute to your overall discount:

- Roof covering: Material type and Florida Building Code compliance. FBC-approved coverings installed after the 2002 code adoption earn the highest rating. Impact-resistant materials earn additional credits

- Roof deck attachment: How the plywood or OSB sheathing is fastened to the trusses. The inspector accesses the attic to examine fastener type and spacing. Ring-shank 8d nails at 6-inch spacing (Category D) earn the highest discount. Standard 8d nails at 6/12 spacing (Category A) earn minimal credit. Staples (Category B) earn no credit

- Roof-to-wall connections: Hurricane straps, clips, or structural connectors that tie the roof to the wall framing. The categories range from toe-nails (no credit) through clips (moderate credit) to single wraps and double wraps (maximum credit). This is often the highest-value category on the form

- Roof geometry: Hip roofs (sloped on all four sides) resist wind significantly better than gable roofs because wind flows over them rather than catching against flat gable ends. A fully hipped roof earns a higher rating than a partially hipped or fully gabled roof

- Secondary water barrier: A sealed membrane over the entire roof deck that prevents water intrusion if the primary covering is lost. This feature earns a substantial credit because it eliminates the interior water damage that accounts for 60-70% of the dollar value of hurricane roof claims

- Opening protection: Hurricane shutters, impact-resistant windows and doors, or storm panels that protect all openings. All openings must be protected to receive full credit. Partial protection receives reduced credit

- Wall construction: Reinforced concrete block (CBS), poured concrete, or other wind-resistant wall systems. Most South Florida homes are CBS construction and qualify for this credit

Wind Mitigation Inspection Costs and ROI

| Item | Cost | Annual Savings | Payback Period |

|---|---|---|---|

| Wind mitigation inspection | $75-$150 | $400-$981 (average) | 1-4 months |

| Hurricane strap installation (retrofit) | $1,500-$3,500 | $200-$600 | 2.5-6 years |

| Secondary water barrier (during re-roof) | $1,000-$2,500 | $150-$400 | 2.5-6 years |

| Impact windows (whole house) | $15,000-$30,000 | $300-$800 | 19-38 years |

| Storm shutters (whole house) | $3,000-$8,000 | $200-$500 | 6-16 years |

| Roof deck re-nailing (during re-roof) | $800-$2,000 | $150-$350 | 2-6 years |

The wind mitigation inspection itself is one of the highest-ROI expenses in homeownership. Even if your home only qualifies for partial credits, the $75-$150 inspection cost pays for itself within months. If the inspection reveals that your home already has features you did not know about, such as hurricane straps installed during original construction or a secondary water barrier applied during a previous re-roof, the savings are essentially free.

Read our complete guide on how your roof affects insurance rates for a deeper dive into each wind mitigation category and how to maximize your credits.

My Safe Florida Home: Up to $10,000 in Free Grant Money

The My Safe Florida Home (MSFH) program is a state-funded grant that helps homeowners pay for hurricane hardening improvements, including many roof-related upgrades. The program received $280 million in funding for the 2025-2026 cycle, with approximately $270 million still available as of February 2026.

How the Grant Works

- 2:1 state match: The state pays $2 for every $1 the homeowner spends on eligible improvements. This means a homeowner who spends $5,000 receives $10,000 from the state, totaling $15,000 in improvements

- $10,000 maximum: The state contribution is capped at $10,000. Low-income homeowners (at or below 200% of the Federal Poverty Level) may receive up to $10,000 with no homeowner match required

- Free inspection: Every approved applicant receives a free comprehensive wind mitigation inspection to identify eligible improvements on their specific property

- Eligible improvements: Roof deck attachment upgrades, secondary water barrier, roof-to-wall connections (hurricane straps), gable end bracing, opening protection (shutters, impact windows, reinforced doors)

Why You Should Apply Now

The legislature has NOT approved new funding for 2027 or beyond. While $270 million remains available, demand is increasing rapidly as awareness of the program grows. Application volume increased 40% in January 2026 compared to the same period in 2025, driven largely by media coverage of the insurance rate decreases. Homeowners who apply now have the best chance of receiving funds before the current allocation is exhausted.

A homeowner who combines the MSFH grant with a roof replacement can reduce their out-of-pocket cost by up to $10,000 while simultaneously earning insurance premium reductions that persist for the life of the new roof. The grant pays for the improvement once. The insurance savings pay you back every year.

Shopping the Market: How 17 New Carriers Change the Game

The influx of 17 new insurance carriers into Florida since the 2022 reforms has created a competitive environment that did not exist even two years ago. For homeowners, this competition translates directly into lower premiums and more options.

How to Shop Effectively in 2026

- Get at least 4-5 quotes: With 17 new carriers plus established companies, there is significant rate variation. One carrier might quote $4,500 while another quotes $3,200 for the identical property and coverage

- Present your wind mitigation report: Every carrier applies wind mitigation credits differently. The same wind mitigation report can produce savings ranging from $300 to $1,200 depending on the carrier's rating model

- Use an independent agent: Independent insurance agents represent multiple carriers and can shop the market on your behalf. They are compensated by the carrier, not by you, so their service costs you nothing

- Compare deductible options: The 2026 market offers more deductible flexibility than previous years. Increasing your hurricane deductible from 2% to 5% can reduce your premium by 15-25%, though you accept more out-of-pocket risk

- Ask about new-roof discounts: Some carriers offer additional discounts beyond wind mitigation credits for roofs less than 5 years old. These "new roof" discounts stack on top of the standard wind mitigation credits

- Check financial stability ratings: New carriers may offer aggressive pricing, but verify their AM Best rating or Demotech rating to ensure they can pay claims after a major storm

Carriers to Request Quotes From

The following carriers have been actively writing new policies in Miami-Dade and Broward counties with competitive rates as of early 2026: Citizens Property Insurance, Universal Insurance, Heritage Insurance, Slide Insurance, TypTap Insurance, Safepoint Insurance, FedNat Insurance, Security First Insurance, and Monarch National Insurance. An independent agent can access all of these plus additional carriers.

What Miami-Dade Homeowners Should Do Right Now

The convergence of rate decreases, new legislation, grant availability, and increased carrier competition creates a narrow window of opportunity that is unprecedented in the past decade. Here is a prioritized action plan for Miami-Dade homeowners who want to maximize every dollar of savings:

Step 1: Get a Free Roof Inspection

Before you can maximize insurance savings, you need to understand the current condition and features of your roof. A professional inspection will identify:

- Current roof condition and estimated remaining useful life

- Existing wind mitigation features you may already qualify for credits on (many homeowners have features they do not know about)

- Specific upgrades that would earn the highest insurance premium reductions for the lowest cost

- Whether your roof qualifies for the HB 815 protections effective July 2026

- The most cost-effective path to maximizing your savings, whether that is a simple wind mitigation inspection, targeted improvements, or a full roof replacement

At Extreme Roofing Inc., we provide comprehensive roof inspections at no cost. Our inspectors evaluate your roof specifically for insurance savings potential and provide a written report detailing every available improvement and its estimated premium impact. Call 305-225-1535 or schedule online.

Step 2: Schedule a Wind Mitigation Inspection

If you have never had a wind mitigation inspection, or if your last one is more than five years old, schedule one immediately. This single step, costing $75 to $150, could save you $400 to $981 per year in premiums starting at your next renewal. The inspection takes approximately 45 minutes to an hour, and the resulting OIR-B1-1802 form is accepted by every insurance carrier in Florida.

Step 3: Apply for My Safe Florida Home

Visit the My Safe Florida Home website and submit your application. The program provides a free inspection, identifies eligible improvements, and funds up to $10,000 in upgrades through the 2:1 matching grant. With no guaranteed funding for 2027, waiting is a risk.

Step 4: Shop Your Insurance

With 17 new carriers in the Florida market, competition is at its highest level since 2017. Get quotes from at least four to five carriers in addition to Citizens. Present your wind mitigation report and any roof upgrades to each carrier to ensure you receive full credit for every feature.

Step 5: Consider Timing Your Roof Replacement

If your roof is approaching the 15-year mark or showing signs of deterioration, 2026 is an exceptionally favorable year for replacement:

- Grant money is available through My Safe Florida Home (up to $10,000 toward your roof hardening improvements)

- Insurance rates are dropping, so your new roof's premium reduction stacks on top of already-reduced market rates

- Multiple carriers are competing for business, rewarding homeowners who invest in quality roofs with the most aggressive pricing

- HB 815 protections take effect July 1, 2026, giving new roofs long-term protection against age-based non-renewals

- Material costs have stabilized after the supply chain disruptions of 2021-2023 that inflated roofing material prices by 30-50%

- Contractor availability is strong outside of hurricane season. January through May is the optimal window for roof replacement in South Florida

Comparing 2026 to Previous Years: Why This Window Matters

To appreciate the significance of the current moment, consider where Florida homeowners were in recent years and how rapidly the landscape has changed:

- 2019: Average premium $2,350. Market stable but showing early signs of stress from litigation and assignment of benefits (AOB) abuse

- 2020: Average premium $2,560. Six carriers left the Florida market entirely. Rate increases of 15-30% statewide. COVID-19 disrupted the construction industry

- 2021: Average premium $3,020. Hurricane Ida losses rippled through global reinsurance markets. Additional carriers exited. Material costs surged 25-40% due to supply chain disruptions

- 2022: Average premium $3,810. Litigation costs peaked. Citizens grew to 1.4 million policies, its largest book ever. Emergency legislative session called in December

- 2023: Average premium $4,231. Highest in the nation by a wide margin. Some coastal homeowners paying $8,000-$15,000 annually. Private market options severely limited

- 2024: Average premium $4,100. First year of stabilization. Tort reform effects beginning to materialize. New carriers entering. Rate increases slowed to 0-5%

- 2025: Average premium $3,800. Private market rates begin declining meaningfully. My Safe Florida Home funded at $280 million. Citizens depopulation accelerates

- 2026: Average premium projected $3,300-$3,500. Citizens rate decrease. 17 new carriers competing. Grant money available. HB 815 protections approaching

The trend is clear and the momentum is strong, but the magnitude of available savings is largest right now because you can combine a one-time market correction (the rate decrease) with permanent structural improvements (roof upgrades and wind mitigation credits). Homeowners who act in 2026 lock in a lower baseline premium that compounds favorably for years to come.

Common Mistakes That Cost Homeowners Money

Even with the favorable 2026 environment, many homeowners leave significant savings on the table through avoidable mistakes:

- Not getting a wind mitigation inspection at all: This is the most common and most costly mistake. The inspection costs $75-$150 and saves an average of $981 per year. There is no legitimate reason not to get one

- Having an outdated wind mitigation report: If your report is more than five years old, or if you have made improvements since the last inspection, you may be missing credits. Get an updated inspection

- Not shopping multiple carriers: Rate variation between carriers can be $500 to $2,000 or more for the same property and coverage. Getting only one quote leaves money on the table

- Ignoring the MSFH grant: Free money is available, but it requires an application. Many homeowners do not know the program exists or assume they will not qualify. Check eligibility and apply

- Waiting for hurricane season: Replacing your roof during hurricane season (June to November) means higher contractor demand, longer wait times, and the risk of a storm hitting before the work is complete. The best time to replace a roof in Florida is January through May

- Choosing the cheapest roof material without considering insurance impact: A $12,000 shingle roof may save $8,000 upfront compared to a $20,000 metal roof, but the metal roof's insurance savings of $600-$1,500 per year close that gap within 5-13 years and then generate net positive savings for the remaining 30-60 years of its lifespan

The Bottom Line: 2026 Is the Year to Act

The Florida insurance market has not offered this combination of favorable conditions in over a decade. Rates are dropping for the first time since 2015. Seventeen new carriers are competing aggressively for your business. State grant money is available for roof improvements through a program that may not be funded again. New legislation protects homeowners with maintained roofs from arbitrary non-renewals based on roof age alone.

Homeowners who take action now, combining the market rate decrease with strategic roof improvements and wind mitigation documentation, will lock in savings that compound year after year for the life of their roof. The homeowner who replaces a 17-year-old shingle roof with a standing seam metal roof, obtains a full wind mitigation report, takes advantage of the MSFH grant, and shops three to five competing carriers could realistically reduce their annual premium from $6,000 to $3,200, a savings of $2,800 per year that persists and compounds.

Do not wait for the next hurricane season to force your hand. Do not wait for the MSFH grant to run out of funding. Do not wait for the 17 new carriers to finish their aggressive pricing phase. The best time to invest in your roof and your insurance savings is right now, before you need to.

Call 305-225-1535 for a free estimate or [schedule your consultation online](/free-estimate).

Frequently Asked Questions

Are Florida home insurance rates really going down in 2026?

Yes. Citizens Property Insurance Corporation approved its first rate decrease since 2015, with an average reduction of 13.2% statewide. Miami-Dade County homeowners are seeing a 14.0% average decrease, and Broward County is seeing 14.1%. Beyond Citizens, 17 new private insurance carriers have entered the Florida market since the 2022 tort reforms, driving additional competition and rate reductions in the private market ranging from 5% to 18% depending on the carrier and region.

How much will my insurance decrease in Miami-Dade in 2026?

Citizens policyholders in Miami-Dade County are receiving an average 14.0% rate decrease, which translates to approximately $630-$840 in annual savings on a typical policy. Private market decreases vary by carrier but range from 5% to 18%. However, the market rate decrease is only part of the picture. Combining it with a roof upgrade and wind mitigation inspection can add another 20-45% in premium reductions, bringing total potential savings to $1,400-$2,600 per year on a $6,000 policy.

Can I stack roof savings on top of the 2026 rate decrease?

Yes. The 2026 market rate decrease and roof-based insurance discounts are independent of each other and fully stackable. The market decrease applies to your base premium, while wind mitigation credits and new roof discounts are applied on top of that reduced base. Additionally, the My Safe Florida Home program offers grants up to $10,000 for roof hardening improvements through a 2:1 state match, further reducing your out-of-pocket costs for upgrades that earn permanent premium reductions.

What roof improvements give the biggest insurance discount?

The highest-impact improvements are: standing seam metal roofing (15-25% premium reduction), hurricane strap installation or upgrade (10-30% reduction), secondary water barrier over the full roof deck (5-10% reduction), and a complete wind mitigation inspection documenting all features ($75-$150 cost, average savings of $981 per year). The wind mitigation inspection is the single highest-ROI step because it costs almost nothing and can unlock hundreds to thousands in annual savings, even without any physical improvements.

Is 2026 a good time to replace my roof in Florida?

2026 is arguably the best time in over a decade to replace your roof in Florida. Insurance rates are dropping, meaning your new roof discount stacks on top of an already-reduced premium. My Safe Florida Home grants are available (up to $10,000) but the legislature has not approved new funding for 2027. Seventeen new insurance carriers are competing for business and rewarding homes with quality roofs. HB 815, effective July 1, 2026, protects new roofs from age-based non-renewals. Material costs have stabilized, and contractor availability is strong during the January-to-May window before hurricane season.

Need Roofing Help?

Whether you need an inspection, repair, or full replacement, our team of licensed roofing professionals is ready to help. Serving South Florida since 2004.

Related Articles

My Safe Florida Home Grant 2026: Get Up to $10,000 for Roof Hardening (Before Funding Runs Out)

The My Safe Florida Home program has $270 million available for roof hardening grants up to $10,000, but the legislature has not approved new funding for 2027. Learn how to apply and maximize your grant.

Read More

How re-roofing your Florida home triggers major insurance savings through wind mitigation credits. Covers the OIR-B1-1802 form, credit categories, average savings of $800-$2,500/year, and the inspection process.

Read More

Discover why standing seam metal roofing is Miami's premium residential choice. Learn about benefits, costs, installation, hurricane ratings, energy efficiency, and long-term value of concealed-fastener metal roofing systems.

Read More