My Safe Florida Home Grant 2026: Get Up to $10,000 for Roof Hardening (Before Funding Runs Out)

How to Get $10,000 From Florida for Your Roof Upgrade in 2026

The My Safe Florida Home program has $280 million in funding for the 2025-2026 cycle, with roughly $270 million still available as of February 2026. This is a state-funded grant program that pays up to $10,000 toward hurricane hardening improvements on your home, including roof deck re-nailing, secondary water barriers, roof-to-wall strap upgrades, and opening protection. Eligible Florida homeowners are getting $10,000 grants for work that directly unlocks insurance premium reductions averaging $981 per year on top.

The catch is that the Florida legislature has NOT approved new funding for 2027 or beyond. The current allocation could be the last for the foreseeable future, and demand is surging. I've been telling every eligible Miami client to apply immediately because the window is narrowing fast.

This post covers exactly how to qualify for the grant, which hurricane hardening improvements are covered, how to apply successfully, and how to combine the grant with a full roof replacement to maximize both the grant money and the insurance savings.

What Is the My Safe Florida Home Program?

My Safe Florida Home (MSFH) is a state-funded hurricane mitigation incentive program administered by the Florida Division of Emergency Management (FDEM). Originally created in 2006 after the devastating 2004-2005 hurricane seasons (when Hurricanes Charley, Frances, Ivan, and Jeanne caused over $45 billion in insured losses), the program was defunded in 2009 during the Great Recession as the state slashed non-essential spending.

The program remained dormant for over a decade while Florida homeowners endured the worst insurance crisis in state history. Premiums tripled. Carriers exited the market. Citizens Property Insurance swelled to 1.4 million policies. It was not until the comprehensive insurance reform package of 2022 that the legislature recognized what actuaries and emergency management professionals had been saying for years: strengthening homes against hurricanes is the most effective and most cost-efficient way to reduce insurance costs at scale.

Governor DeSantis signed the renewed program into law with an initial appropriation of $150 million, which was subsequently increased to $280 million for the 2025-2026 funding cycle based on overwhelming demand and demonstrated results from the initial round of grants.

The Program's Dual Mission

The program has a dual purpose that benefits both individual homeowners and the state as a whole:

- Reduce hurricane damage: By funding structural improvements that make homes more resistant to high winds and wind-driven rain, the program directly reduces the number and severity of insurance claims after hurricanes. Every home hardened is a claim prevented

- Lower insurance costs: By creating a measurable reduction in insured losses across the state, MSFH allows carriers to reduce premiums. The improvement to the risk pool benefits all policyholders, not just those who receive grants

Every dollar the state invests in MSFH generates an estimated $3 to $7 in reduced insurance claims over the following decade, according to actuarial analysis by the Florida Office of Insurance Regulation. This makes it one of the most cost-effective disaster mitigation programs in the nation and one of the most effective uses of state funds for direct taxpayer benefit.

Why 2026 Is the Critical Year

The current $280 million funding cycle covers 2025-2026. As of the most recent legislative session, no new appropriation has been approved for 2027 or beyond. While advocates including insurance industry groups, emergency management officials, and consumer protection organizations are lobbying for continued funding, there is no guarantee. Budget priorities shift. Political dynamics change. New crises emerge.

Homeowners who apply in 2026 have access to a well-funded program with significant available capacity. Homeowners who wait until 2027 may find the program unfunded, oversubscribed, or fundamentally restructured. The prudent action is to apply now while funding is guaranteed and available.

Eligibility Requirements: Do You Qualify?

Not every Florida homeowner qualifies for MSFH. The program has specific eligibility criteria designed to target the homes that would benefit most from hurricane hardening improvements. Understanding these requirements before you apply saves time and prevents the frustration of a rejected application.

Eligibility Requirements Checklist

| Requirement | Details | Documentation Needed |

|---|---|---|

| Property type | Site-built single-family home (no mobile homes, condos, or townhomes in HOA-maintained structures) | Property appraiser records |

| Homestead exemption | Property must have active homestead exemption filed with the county | County property appraiser confirmation |

| Insured value | Home insured value must be $500,000 or less (based on insurance declarations page, not market value) | Current insurance declarations page |

| Construction date | Home must have been built before 2008 (pre-current Florida Building Code adoption) | Building permit records or property appraiser data |

| Location | Must be located in Florida (program is statewide, not limited to coastal counties) | Property address |

| Owner-occupied | Must be the applicant's primary residence, not an investment or rental property | Homestead exemption serves as proof |

| Current insurance | Must have an active homeowner's insurance policy on the property | Insurance declarations page |

| No prior MSFH grant | Cannot have received a previous MSFH grant on the same property | Self-attestation plus program records verification |

Common Disqualifiers to Watch For

Several types of properties and situations are NOT eligible, and these disqualifiers are strictly enforced:

- Manufactured or mobile homes: These have a separate mitigation program administered by the Florida Division of Emergency Management. Site-built homes only

- Rental and investment properties: Investment properties do not qualify even if you own them outright. The program targets primary residences only

- Homes valued above $500,000: The insured value cap is strict and is based on the dwelling coverage amount on your insurance declarations page, not the market value or appraised value of the home. A home with a market value of $600,000 but an insured value of $450,000 would qualify

- Homes built after 2007: These were built under the current Florida Building Code (which was significantly strengthened after the 2004-2005 hurricane seasons) and are presumed to already have adequate hurricane-resistant features

- Condominiums with HOA-managed roofs: If the homeowners association is responsible for the roof structure and covering, the individual unit owner cannot apply. The HOA would need to pursue commercial hardening options

- Homes with prior MSFH grants: The program allows one grant per property address. If a previous owner received an MSFH grant on the property, it is not eligible for a second grant

Income-Based Tiers

The program has two tiers based on household income, and understanding which tier you fall into affects your out-of-pocket costs:

- Standard tier: Homeowners with household income above 200% of the Federal Poverty Level receive 2:1 matching, meaning the state pays $2 for every $1 the homeowner spends on eligible improvements, up to a $10,000 state contribution. This means you spend $5,000 and the state contributes $10,000 for a total of $15,000 in improvements

- Low-income tier: Homeowners at or below 200% of the Federal Poverty Level may receive up to $10,000 in grant funds with no homeowner match required. This effectively provides free hurricane hardening improvements for qualifying low-income homeowners

For a family of four in 2026, 200% of the Federal Poverty Level is approximately $62,400 in annual household income. Homeowners below this threshold should apply under the low-income tier for maximum benefit. Documentation of income is required, typically through recent tax returns or pay stubs.

What Improvements Are Covered by the Grant

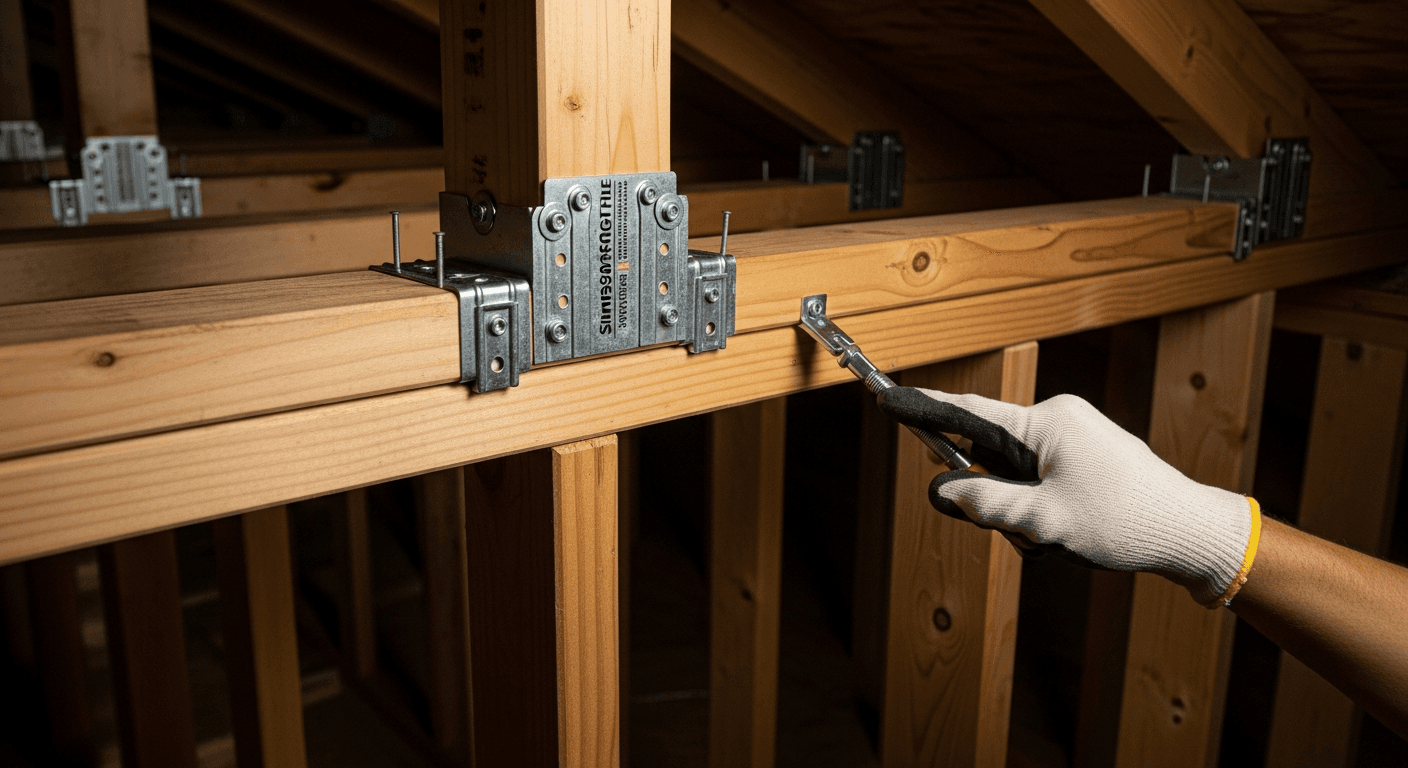

The MSFH grant covers specific hurricane hardening improvements identified through the program's inspection process. Not every home improvement qualifies. The covered improvements are limited to items that directly reduce wind damage risk as documented on the standard wind mitigation inspection form.

Eligible Improvements: Typical Costs vs. Grant Coverage

| Improvement | Typical Cost | Grant Coverage (2:1 Match) | Your Out-of-Pocket | What It Does |

|---|---|---|---|---|

| Roof deck attachment upgrade | $3,000-$6,000 | Up to $4,000 | $1,000-$2,000 | Re-nailing roof sheathing with ring-shank 8d nails at 6" spacing to prevent deck uplift |

| Secondary water barrier (SWB) | $2,000-$5,000 | Up to $3,333 | $667-$1,667 | Self-adhering modified bitumen membrane over entire roof deck for backup waterproofing |

| Roof-to-wall connections | $2,500-$5,000 | Up to $3,333 | $833-$1,667 | Hurricane straps or clips connecting roof trusses to wall top plates to prevent roof separation |

| Gable end bracing | $1,500-$3,500 | Up to $2,333 | $500-$1,167 | Structural bracing for gable-end walls to prevent inward or outward collapse during high winds |

| Opening protection (shutters) | $3,000-$12,000 | Up to $6,667 | $1,000-$5,333 | Hurricane shutters or impact-rated covers for all windows and doors |

| Opening protection (impact windows) | $10,000-$30,000 | Up to $6,667 | $3,333-$23,333 | Impact-resistant windows and doors replacing all standard openings |

| Exterior door reinforcement | $800-$2,500 | Up to $1,667 | $267-$833 | Hurricane-rated entry doors and reinforced garage doors |

| Roof covering upgrade | $8,000-$25,000 | Up to $6,667 | $1,333-$18,333 | FBC-compliant roof covering when combined with other eligible improvements |

Important : The $10,000 maximum applies to the total state contribution across ALL improvements combined, not per individual improvement. The 2:1 match structure means you can access up to $15,000 in total improvements ($5,000 from you plus $10,000 from the state).

Which Improvements Offer the Best ROI

Not all improvements are created equal when it comes to bang for your buck. If you are trying to maximize your grant dollars, focus on improvements that deliver the highest insurance premium reduction per dollar spent after the grant offset.

The three highest-ROI improvements for most South Florida homes are:

- Roof-to-wall connections (hurricane straps): This single improvement can earn $300-$700 per year in insurance savings at a net cost of $833-$1,667 after the grant. The payback period is often less than 3 years

- Roof deck attachment upgrade: Re-nailing the deck with ring-shank nails earns $250-$550 per year in savings at a net cost of $1,000-$2,000 after the grant. Payback in 2-4 years

- Secondary water barrier: Earns $200-$450 per year at a net cost of $667-$1,667 after the grant. Payback in 2-4 years

The key insight is that roof-related improvements (items 1-3 above) generally offer better ROI than opening protection because they cost less to install, they benefit from the grant matching more efficiently, and they earn credits in the most heavily weighted categories on the wind mitigation form.

Insurance Savings from Each Improvement Type

Every eligible MSFH improvement earns a specific category of insurance premium reduction through the wind mitigation inspection system. Here is what each improvement is worth in annual premium savings, based on documented data from major Florida carriers:

| Improvement | Average Annual Insurance Savings | 10-Year Cumulative Savings | Premium Impact Category |

|---|---|---|---|

| Roof deck attachment (A to D upgrade) | $250-$550 | $2,500-$5,500 | Wind mitigation Form OIR-B1-1802 Section 2 |

| Secondary water barrier | $200-$450 | $2,000-$4,500 | Wind mitigation Form Section 5 |

| Roof-to-wall connections (clips to straps) | $300-$700 | $3,000-$7,000 | Wind mitigation Form Section 3 |

| Gable end bracing | $100-$250 | $1,000-$2,500 | Structural improvement (varies by carrier) |

| Opening protection (all openings) | $250-$600 | $2,500-$6,000 | Wind mitigation Form Section 6 |

| Combined all improvements | $981 average | $9,810 | Full wind mitigation package |

The most impactful single improvement for insurance savings is typically the roof-to-wall connection upgrade (hurricane straps), which earns credits in one of the highest-weighted categories on the wind mitigation form. The jump from toe-nail connections (no credit) to single-wrap hurricane straps (significant credit) can save $300 to $700 per year on its own.

When combined with roof deck attachment and secondary water barrier upgrades during a re-roofing project, the total savings package is maximized because all three improvements share the same labor overhead of exposing the roof deck during the re-roof.

ROI Calculation: What You Actually Save After the Grant

Understanding the true ROI of an MSFH-funded improvement requires accounting for the grant offset, the ongoing insurance savings, and any increase in home value. The numbers are compelling.

ROI Example 1: Full Roof Hardening Package

| Line Item | Amount |

|---|---|

| Total improvement cost (deck + SWB + straps + bracing) | $12,000 |

| MSFH grant (2:1 match on your $4,000) | -$8,000 |

| Your out-of-pocket cost | $4,000 |

| Annual insurance savings | $981 |

| Payback period | 4.1 years |

| 10-year net savings | $5,810 |

| Estimated home value increase | $5,000-$10,000 |

| Total 10-year ROI | $10,810-$15,810 (170%-295%) |

ROI Example 2: Roof-to-Wall Connections Only

| Line Item | Amount |

|---|---|

| Total improvement cost (hurricane straps retrofit) | $3,500 |

| MSFH grant (2:1 match on your $1,167) | -$2,333 |

| Your out-of-pocket cost | $1,167 |

| Annual insurance savings | $500 |

| Payback period | 2.3 years |

| 10-year net savings | $3,833 |

ROI Example 3: Full Roof Replacement + Hardening (Maximum Value)

| Line Item | Amount |

|---|---|

| New [metal roof](/services/metal-roofs) installed | $22,000 |

| Hardening improvements (SWB + deck + straps) | $3,500 (added during re-roof at reduced cost) |

| Total project cost | $25,500 |

| MSFH grant (maximum $10,000) | -$10,000 |

| Your out-of-pocket cost | $15,500 |

| Annual insurance savings (full package) | $2,200 |

| Payback period | 7.0 years |

| 10-year net savings | $6,500 |

| Estimated home value increase | $15,000-$25,000 |

| Total 10-year ROI (including home value) | $21,500-$31,500 (39%-103%) |

Even in the most expensive scenario (full metal roof replacement), the investment turns positive within 10 years when accounting for the MSFH grant, insurance savings, and home value increase. For a roof that will last 40-70 years, the lifetime ROI is extraordinary.

How to Apply: Step-by-Step Process

The application process has several stages and each one has specific requirements. Understanding the full process in advance prevents delays and ensures your application moves smoothly through the system from start to finish.

Step 1: Verify Your Eligibility

Before applying, confirm that your home meets all eight eligibility criteria listed in the checklist above. The most common reasons for application rejection are:

- Insured value exceeding $500,000 (check your insurance declarations page, not Zillow)

- Home built after 2007 (check your county property appraiser records or original building permit)

- Homestead exemption not filed or not current

- Property is not the applicant's primary residence

Take 15 minutes to verify these items before starting the application. It will save you weeks of processing time if a disqualification is caught early.

Step 2: Submit Your Online Application

Visit the My Safe Florida Home website (mysafefloridahome.com) and complete the online application. You will need to provide:

- Property address and parcel number (available from your county property appraiser website)

- Proof of homestead exemption (printout from county property appraiser or tax records)

- Current insurance declarations page showing insured value is $500,000 or less

- Household income documentation for low-income tier applicants (tax returns, W-2s, or pay stubs)

The application takes approximately 20 to 30 minutes to complete. After submission, you will receive a confirmation number and email. Keep this confirmation for your records.

Step 3: Schedule Your Free Inspection

Once your application is approved (typically 2-4 weeks), the program assigns a licensed inspector to evaluate your home at no cost to you. This is a comprehensive wind mitigation inspection that identifies every eligible improvement for your specific property.

The inspection typically takes 1 to 2 hours and covers:

- Roof covering type and condition: Material identification, age estimation, and FBC compliance

- Roof deck attachment method: Requires attic access to examine fastener types and spacing

- Roof-to-wall connection type: Attic examination of how trusses connect to wall top plates

- Gable end configuration and bracing: Assessment of gable walls and existing bracing

- Opening protection status: Every window, door, and garage door evaluated

- Wall construction type: CBS, frame, or other construction identification

- Roof geometry: Hip percentage measurement for wind resistance rating

Step 4: Review Your Inspection Report

The inspector provides a detailed report listing every eligible improvement for your specific home, its estimated cost, and the grant amount available for that improvement. This report is your roadmap. You are not obligated to complete all recommended improvements. You can select the improvements that offer the best return for your budget and priorities.

Review the report carefully and consider:

- Which improvements earn the highest insurance savings per dollar of your out-of-pocket cost

- Whether combining improvements with a planned roof replacement reduces overall costs

- The total grant amount you can access based on the improvements you select

Step 5: Select a Licensed Contractor

You must use a licensed Florida roofing contractor to perform the improvements. The contractor must meet all of the following requirements:

- Hold a valid CCC or CRC Florida roofing license (verify at myfloridalicense.com)

- Carry active workers' compensation and general liability insurance

- Be registered with the MSFH program as an approved contractor

- Provide a written estimate that itemizes each improvement separately with specific costs

At Extreme Roofing Inc., we are fully licensed (Florida CCC license), insured, and experienced with the MSFH grant process. We have completed dozens of MSFH-funded projects throughout Miami-Dade and Broward counties and can handle the entire process from inspection coordination to grant paperwork to final inspection. Call 305-225-1535 for a free consultation.

Step 6: Submit Contractor Estimate for Grant Approval

Your contractor submits the itemized estimate to MSFH for grant approval. The program reviews the estimate to confirm that all proposed improvements are eligible, costs are within reasonable ranges for the market, and the contractor is properly licensed and registered. This review typically takes 2 to 4 weeks.

Step 7: Complete the Work

Once the grant is approved, your contractor performs the improvements. The work must be completed within 120 days of grant approval. All improvements must be installed according to current Florida Building Code specifications and must pass a final inspection.

Step 8: Final Inspection and Grant Disbursement

After the work is complete, MSFH sends an inspector to verify that all improvements were installed correctly and match the approved scope of work. Upon passing the final inspection, the grant funds are disbursed directly to the contractor, and you pay only your share (the homeowner match portion). You do not need to front the state's portion of the cost.

Step 9: Update Your Wind Mitigation Report

This step is critical and often overlooked. After the improvements are complete, obtain an updated wind mitigation inspection report (OIR-B1-1802 form) reflecting all new features. Submit this updated report to your insurance company to receive the full premium reduction. The annual savings begin immediately upon your next policy renewal. Without this updated report, your insurer will not know about the improvements and will not apply the discounts.

Timeline: How Long Does the Entire Process Take?

The complete MSFH process from application submission to grant disbursement typically takes 3 to 6 months. Here is a realistic timeline based on current processing speeds:

- Application submission to approval: 2-4 weeks (initial eligibility review)

- Inspection scheduling and completion: 2-4 weeks after approval (depends on inspector availability in your area)

- Review inspection report and select contractor: 1-2 weeks (your decision time)

- Contractor estimate submission and grant approval: 2-4 weeks (program review)

- Construction completion: 1-3 weeks for roof hardening work (longer if combined with full re-roof)

- Final inspection and grant disbursement: 2-4 weeks after work is complete

- Updated wind mitigation report and insurance submission: 1-2 weeks (your action)

Total estimated timeline : 11 to 23 weeks (approximately 3 to 6 months)

Homeowners who begin the process in February or March 2026 can realistically have their improvements completed, their grant disbursed, and their insurance savings activated before hurricane season begins on June 1. This is the ideal timeline and the one we recommend.

Tips for Maximizing Your Grant Value

After working with dozens of MSFH applicants across Miami-Dade and Broward counties, here are the strategies that consistently produce the best outcomes:

Tip 1: Combine Multiple Improvements in a Single Project

The grant covers up to $10,000 in state funds across all improvements combined. Homeowners who combine multiple improvements in a single project maximize the total grant value and minimize total labor costs. For example, combining roof deck attachment ($4,000) with secondary water barrier ($3,000) and hurricane straps ($3,500) totals $10,500 in improvements. Under the 2:1 match, you pay $3,500 and the state covers $7,000. Each improvement was installed in a single mobilization, reducing overhead costs compared to doing them separately.

Tip 2: Time It with a Planned Roof Replacement

If your roof is due for replacement within the next 3-5 years, timing the MSFH improvements to coincide with your re-roofing project saves significant labor costs. Secondary water barrier installation and roof deck attachment upgrades are dramatically cheaper when performed during a re-roof because the roof covering is already removed, providing direct access to the deck. A standalone SWB installation might cost $4,000 to $5,000 because it requires removing and reinstalling the existing roof covering. Adding SWB during a re-roof costs only $1,500 to $2,500 because the deck is already exposed. The same logic applies to deck re-nailing and hurricane strap installation.

Tip 3: Apply and Get Inspected Before Hurricane Season

Inspector availability tightens significantly from June through November as demand surges during hurricane season and after any named storms. Apply in the first quarter of the year to secure the fastest inspection scheduling and the widest contractor availability for the subsequent work.

Tip 4: Choose a Contractor Experienced with the MSFH Process

The grant paperwork, compliance requirements, and inspection coordination can slow down contractors who have never worked with the program. Choosing a contractor experienced with MSFH grants reduces delays, ensures the estimate is formatted correctly for approval, and helps the work pass the final inspection on the first attempt. Ask your contractor how many MSFH projects they have completed.

Tip 5: Document Everything Thoroughly

Keep copies of all inspection reports, contractor estimates, grant approval letters, construction progress photos, completion certificates, and final inspection results. You will need these documents to update your wind mitigation report, file insurance claims in the future, demonstrate improvements to prospective buyers if you sell your home, and respond to any insurer inquiries about your roof's condition.

Tip 6: Stack All Available Programs and Credits

MSFH is not the only assistance available. Miami-Dade County occasionally offers additional hardening grants through local emergency management programs. The FHA 203(k) renovation loan allows you to roll improvement costs into your mortgage at favorable interest rates. Some insurance carriers offer additional premium credits for completing verified hardening improvements beyond what the standard wind mitigation form captures. And the 2026 market conditions mean the insurance rate decreases stack on top of your MSFH-funded improvements, compounding your total savings.

The Urgency Factor: Why Waiting Is a Genuine Risk

Several converging factors create genuine urgency around the MSFH program in 2026. This is not manufactured urgency. These are structural realities that make the current moment uniquely favorable.

Funding Is Not Guaranteed Beyond 2026

The $280 million appropriation covers the 2025-2026 cycle only. No new funding has been approved for 2027 or beyond. While the program has strong bipartisan support and demonstrated results, legislative priorities shift, budget pressures mount from other state needs, and there is no guarantee that MSFH will be refunded at the same level, or at all. Homeowners who apply now are accessing guaranteed, available funding. Those who wait are gambling on future legislative action that may not materialize.

Demand Is Accelerating Rapidly

Awareness of the MSFH program has grown substantially since its revival, driven by media coverage, insurance agent recommendations, and word-of-mouth from homeowners who have already benefited. The program reported a 40% increase in applications in January 2026 compared to the same period in 2025. As more homeowners learn about the program through coverage of the 2026 rate decreases, the remaining funds will be allocated faster. The $270 million currently available is a large sum, but not unlimited.

Hurricane Season Starts June 1

The improvements funded by MSFH are designed to protect your home during hurricanes. Every month you wait after June 1 is a month your home remains vulnerable to a storm that could cause damage your current roof features cannot withstand. Completing improvements before hurricane season provides both physical protection for your home and family, and insurance savings that begin at your next renewal.

Insurance Rate Decreases May Not Last Forever

While the current trend is downward, insurance markets are inherently cyclical. A major hurricane hitting South Florida, a spike in reinsurance costs, or a change in the legislative framework could reverse the rate trajectory within a single season. Homeowners who lock in low rates by completing hardening improvements now are insulated against future rate increases because their wind mitigation credits are permanent. The credits follow the features, not the market conditions.

Common Mistakes That Waste Grant Money

After guiding dozens of homeowners through the MSFH process, we have seen several recurring mistakes that reduce the grant's value or cause delays. Avoiding these pitfalls ensures you get maximum benefit from the program:

- Not getting the updated wind mitigation report after improvements: This is by far the most costly mistake. Some homeowners complete their MSFH improvements and never schedule an updated wind mitigation inspection. Without the updated OIR-B1-1802 form submitted to your insurer, the improvements exist physically but do not exist in the insurance system. You continue paying the old, higher premium. Schedule the updated inspection within 30 days of project completion

- Choosing the cheapest contractor rather than the most experienced: MSFH projects have specific paperwork, compliance, and inspection requirements. A contractor who submits an incorrectly formatted estimate delays your grant approval by weeks. A contractor who fails the final inspection requires rework at additional cost. Pay a fair price for a contractor who knows the MSFH process

- Applying without verifying eligibility first: Homeowners who submit applications before confirming their insured value, construction date, or homestead status waste 2-4 weeks waiting for a rejection. Verify all eight requirements before you apply

- Doing improvements one at a time instead of combining them: Each mobilization (each time a contractor comes to your property) has a fixed overhead cost for labor, equipment, and setup. Combining roof deck re-nailing, SWB, and hurricane straps in a single project is significantly cheaper than doing them as three separate projects. The grant also maximizes when you bundle improvements to reach the $10,000 cap

- Waiting until hurricane season to start the process: Inspector and contractor availability drops dramatically from June through November. Processing times increase. The risk of a storm interrupting your project increases. Start in the first quarter of the year

- Not shopping insurance after the improvements are complete: Some homeowners complete their improvements, get the updated wind mitigation report, and send it to their existing insurer without shopping alternatives. With 17 new carriers in the market, you may find that a competitor values your improved roof more aggressively than your current carrier. Get at least three quotes with your new report

What Happens After Your Improvements Are Complete

Completing MSFH-funded improvements is the beginning, not the end. To maximize the long-term value of your investment and ensure every dollar of premium reduction is captured:

- Update your wind mitigation inspection immediately: Schedule a new OIR-B1-1802 inspection within 30 days of completion to document all improvements. This is the document your insurer needs to apply the premium discounts you have earned

- Submit the updated report to your insurer in writing: Send the new wind mitigation report to your insurance company and request a formal premium review. Most carriers will apply the new credits at your next renewal. Some will adjust mid-term if the savings are significant

- Shop competing carriers with your new report: Use your updated wind mitigation report to get quotes from at least three to five carriers. The improvements you have made are fully portable between insurance companies. A carrier that would not write your policy before the improvements may now offer highly competitive pricing

- Keep all documentation permanently: Maintain organized copies of the MSFH grant approval letter, contractor estimates, construction progress photos, completion certificates, final inspection results, and updated wind mitigation report. These documents add substantial value when selling your home, as buyers and their insurers will value documented hurricane hardening features

- Schedule annual professional maintenance: Protect your investment with annual professional roof inspections to ensure all improvements remain in good condition and continue earning their full insurance credits year after year. A $300 annual inspection protects a $15,000-$25,000 investment

- Monitor your premium at each renewal: Verify that your insurer continues to apply the correct wind mitigation credits at each renewal. Credits should persist as long as the features exist. If credits are removed without explanation, contact your insurer immediately and provide the documentation

Real Numbers: A Complete Miami-Dade Homeowner Scenario

Let us walk through a complete real-world scenario for a homeowner in Kendall, Miami-Dade County, with a 2001-built CBS home, an 18-year-old architectural shingle roof, and a current insurance premium of $5,800 per year with Citizens Property Insurance.

| Item | Amount |

|---|---|

| Current annual premium (Citizens, 2025) | $5,800 |

| 2026 Citizens rate decrease (14%) | -$812 |

| New premium after market decrease | $4,988 |

| New [metal roof](/services/metal-roofs) with full hardening package | Cost: $25,500 |

| MSFH grant (maximum $10,000) | -$10,000 |

| Out-of-pocket for roof + hardening | $15,500 |

| New roof insurance discount (20%) | -$998 |

| Wind mitigation credits from hardening (additional 15%) | -$598 |

| Shopping to competitive private carrier (additional 8%) | -$271 |

| New annual premium after all actions | $3,121 |

| Total annual savings vs. 2025 | $2,679 |

| Payback on $15,500 investment | 5.8 years |

| 10-year net savings | $11,290 |

| Home value increase from metal roof | $15,000-$25,000 |

| Total 10-year financial benefit | $26,290-$36,290 |

This homeowner spends $15,500 out of pocket (after the $10,000 MSFH grant), saves $2,679 per year in insurance, recoups the investment in under 6 years, and generates over $26,000 in total financial benefit over the following decade. The new metal roof also eliminates the need for another roof replacement for 40 to 70 years, avoids the $18,000-$25,000 cost of a future shingle replacement, and provides superior hurricane protection for the family.

This is the power of combining MSFH grants with the 2026 rate decrease, a new roof, and proactive insurance shopping. Each element alone is valuable. Combined, they are transformative.

Call 305-225-1535 for a free roof inspection and MSFH consultation, or [schedule your appointment online](/free-estimate).

Frequently Asked Questions

Is the My Safe Florida Home program still accepting applications in 2026?

Yes. As of February 2026, the My Safe Florida Home program is actively accepting applications. The program has approximately $270 million remaining from its $280 million 2025-2026 funding cycle. However, the Florida legislature has NOT approved new funding for 2027 or beyond, and application volume has increased 40% year-over-year. Homeowners should apply as soon as possible to secure their grant before funds are exhausted.

What roof improvements are covered by the MSFH grant?

The MSFH grant covers six categories of hurricane hardening improvements: roof deck attachment upgrades (re-nailing sheathing with ring-shank nails at 6-inch spacing), secondary water barrier installation (self-adhering membrane over the entire roof deck), roof-to-wall connection upgrades (hurricane straps and clips), gable end bracing, opening protection (hurricane shutters, impact windows, and reinforced doors), and roof covering upgrades when performed in conjunction with other eligible improvements. All improvements must be performed by a licensed Florida contractor registered with the MSFH program.

How much does the My Safe Florida Home grant actually pay?

The standard grant structure is a 2:1 state match, meaning the state pays $2 for every $1 the homeowner spends on eligible improvements, up to a maximum state contribution of $10,000. For example, if you spend $5,000 on eligible improvements, the state contributes $10,000 for a total of $15,000 in work. Low-income homeowners (household income at or below 200% of the Federal Poverty Level, approximately $62,400 for a family of four in 2026) may receive up to $10,000 with no homeowner match required.

Do I need to replace my entire roof to qualify for the grant?

No. You do not need to replace your entire roof to qualify for the MSFH grant. Many eligible improvements, including hurricane strap installation, gable end bracing, and opening protection, can be performed without touching your existing roof covering. However, roof deck attachment upgrades and secondary water barrier installation are most cost-effective when performed during a full re-roofing project because access to the roof deck is required. If your roof is nearing the end of its useful life, combining a roof replacement with MSFH-funded improvements maximizes both the grant value and your insurance savings.

How long does the My Safe Florida Home process take?

The complete MSFH process from application submission to grant disbursement typically takes 3 to 6 months. The breakdown is approximately 2-4 weeks for application approval, 2-4 weeks for the free inspection, 1-2 weeks for contractor selection and estimate submission, 2-4 weeks for grant approval of the estimate, 1-3 weeks for construction, and 2-4 weeks for final inspection and disbursement. Homeowners who begin in early 2026 can realistically complete the process before hurricane season starts on June 1.

Need Roofing Help?

Whether you need an inspection, repair, or full replacement, our team of licensed roofing professionals is ready to help. Serving South Florida since 2004.

Related Articles

My Safe Florida Home Grant 2026: Get Up to $10,000 for Roof Hardening (Before Funding Runs Out)

The My Safe Florida Home program has $270 million available for roof hardening grants up to $10,000, but the legislature has not approved new funding for 2027. Learn how to apply and maximize your grant.

Read More

Florida insurance rates are dropping for the first time since 2015. Learn how combining market rate decreases with strategic roof upgrades can save Miami homeowners $1,400-$2,600 per year on premiums.

Read More

How re-roofing your Florida home triggers major insurance savings through wind mitigation credits. Covers the OIR-B1-1802 form, credit categories, average savings of $800-$2,500/year, and the inspection process.

Read More