Wind Mitigation & Re-Roofing in Florida: Insurance Savings Guide

The Florida Insurance Savings Most Homeowners Leave on the Table

Most Miami homeowners I work with are shocked when I tell them how much they can save on insurance by installing a new roof and properly filing wind mitigation credits. The typical savings for a Miami home with a new Miami-Dade NOA roof and a complete wind mitigation inspection form runs $900 to $2,500 per year. Over a 10-year period, that's $9,000 to $25,000 in cumulative savings, often recovering 30 to 60 percent of the original roof replacement cost.

The catch is that you have to actually claim the credits. I've seen homeowners replace their roofs with the right products and never get the wind mitigation inspection done, which means they're paying full price on insurance and don't know why. The inspection costs $125 to $175 and unlocks thousands of dollars in annual savings. Skipping it is one of the most expensive mistakes you can make as a Miami homeowner.

This post covers exactly how wind mitigation credits work in 2026, which roof features unlock the biggest discounts, how to get the inspection done right, and what insurance carriers typically offer in Miami-Dade County.

This guide explains exactly how the wind mitigation system works in Florida, what each credit category means, how a new roof earns you the highest possible discounts, and the step-by-step process for getting inspected after your re-roofing project.

What Is a Wind Mitigation Inspection in Florida?

A wind mitigation inspection is a standardized assessment of a home's structural features that resist wind damage during hurricanes and tropical storms. The inspection is documented on the OIR-B1-1802 form (also known as the Uniform Mitigation Verification Inspection Form), which was developed by the Florida Office of Insurance Regulation.

Florida law (Section 627.0629, Florida Statutes) requires insurance companies to provide premium discounts for homes with wind-resistant features verified through this inspection. The law was enacted because Florida's building code . particularly the enhanced requirements adopted after Hurricane Andrew in 1992 . produces homes and roofing systems that demonstrably withstand hurricanes better than older construction.

Who Can Perform a Wind Mitigation Inspection?

Only the following licensed professionals can complete the OIR-B1-1802 form:

- Licensed home inspectors (with wind mitigation certification)

- Licensed general contractors, building contractors, or residential contractors

- Licensed professional engineers

- Licensed architects

The inspection typically costs $75 to $150 and takes 30 to 60 minutes. Given the potential for thousands of dollars in annual savings, it is one of the highest-return investments a Florida homeowner can make.

---

Get your free roofing estimate today. Extreme Roofing Inc. has served South Florida since 2004 with over 20 years of certified expertise. Call 305-225-1535 or request your free estimate online.

---

The OIR-B1-1802 Form: Understanding Each Credit Category

The wind mitigation form evaluates seven specific features of your home. Each feature has multiple possible ratings, and each rating translates to a different insurance discount. Here is what the inspector evaluates and how a new roof impacts each category.

1. Roof Covering

This section identifies the type of roof covering material and the code standard to which it was installed.

Rating options:

- FBC (Florida Building Code): Roof covering installed under permits issued after March 1, 2002 that meets FBC requirements

- Non-FBC: Roof covering installed before FBC adoption or not meeting FBC standards

How a new roof helps: Any new roof installed by a licensed Florida roofing contractor after March 1, 2002, automatically qualifies for the FBC rating. This is the most impactful single credit on the form. Homes with FBC-compliant roof coverings receive the largest premium discount in this category . typically 15% to 30% off the wind portion of the premium.

The critical detail: The form also records the permit date and the installation date. A roof installed in 2024 under the current Florida Building Code (7th Edition, 2023) earns the strongest FBC credit. Older permitted roofs that still meet FBC standards also qualify but may receive slightly lower discounts depending on the insurer.

2. Roof Deck Attachment

This section evaluates how the plywood or OSB roof deck is attached to the trusses or rafters below it.

Rating options (from weakest to strongest):

- A: 6d nails, 6 inches on center (weakest)

- B: 8d nails, 6 inches on center

- C: 8d nails, 6 inches on center at edges and field (reinforced nailing)

- D: Ring-shank nails or stapled with specific patterns (strongest nailed)

- Structural composite: Full plywood or engineered wood systems

How a new roof helps: During a re-roofing project, the existing deck attachment can be evaluated and upgraded. If the tear-off reveals that the deck is attached with 6d nails (Rating A), the roofing contractor can renail the deck with 8d ring-shank nails to achieve a Rating D. This upgrade adds $500 to $1,500 to the project cost but generates significant annual insurance savings.

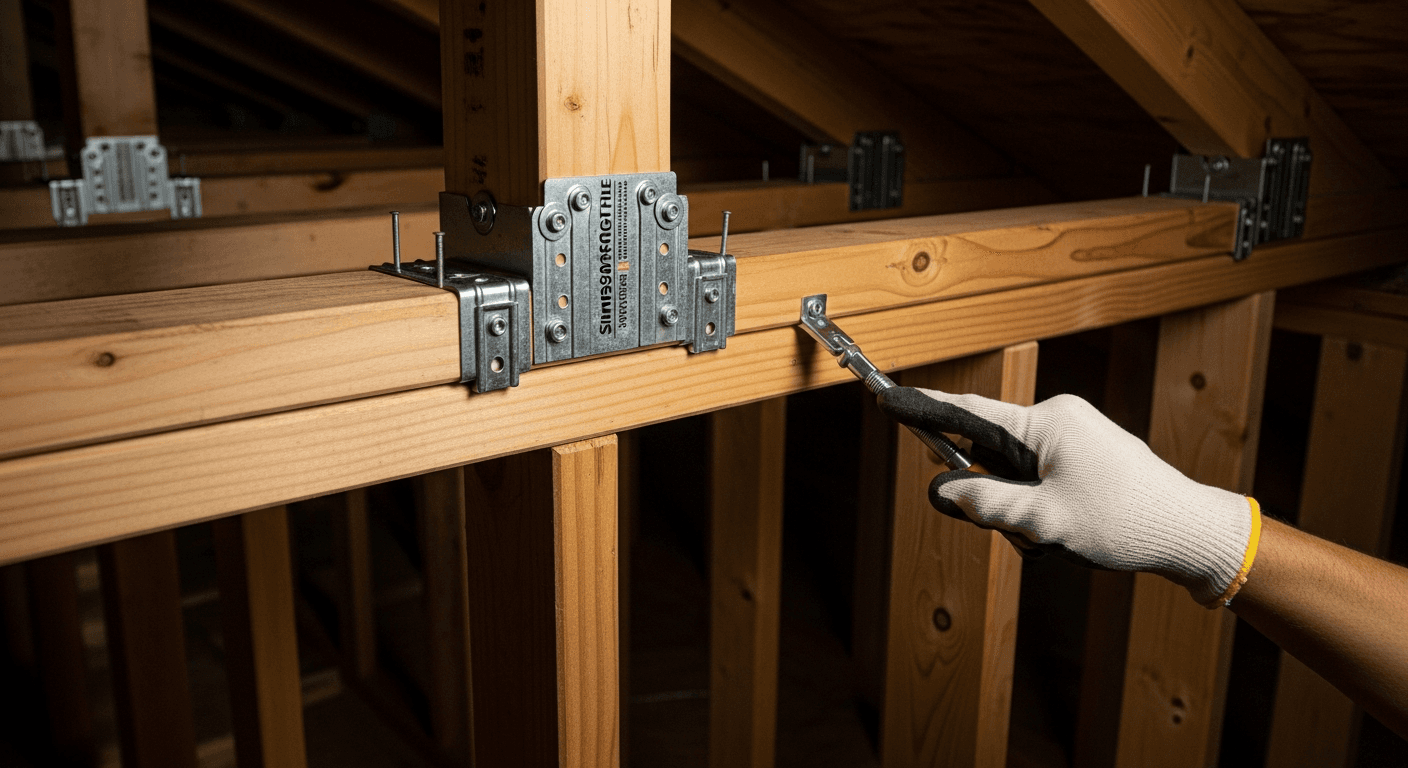

3. Roof-to-Wall Connection

This is the method by which the roof structure (trusses or rafters) is connected to the exterior walls. It is one of the most critical wind resistance features.

Rating options (from weakest to strongest):

- Toe nails: Trusses or rafters attached to the top plate with nails driven at an angle (weakest)

- Clips: Metal clips connecting the truss/rafter to the top plate

- Single wraps: Metal straps that wrap over the top of the truss/rafter and attach to both sides

- Double wraps: Metal straps that wrap over and are nailed on both sides with redundant connections (strongest)

How a new roof helps: While the roof-to-wall connection is not part of the roof covering itself, a re-roofing project provides the opportunity to upgrade connections. When the roof deck is exposed during tear-off, a contractor can install hurricane straps or clips on accessible trusses. Upgrading from toe nails to single wraps or double wraps can yield insurance savings of $300 to $800 per year alone.

4. Roof Geometry

This section records the shape of the roof, which affects its aerodynamic performance during hurricanes.

Rating options:

- Hip roof: All sides slope downward from the ridge (best wind performance)

- Non-hip: Includes gable, flat, gambrel, and other non-hip configurations

How a new roof helps: Roof geometry is determined by the home's architecture and generally does not change during a re-roofing project. However, some gable roofs can be retrofitted with hip-end bracing or gable-end bracing during re-roofing to improve wind performance, though this does not change the geometry classification on the form.

Hip roofs receive the largest discount in this category because they present sloped surfaces to wind from every direction, significantly reducing uplift forces compared to a gable end wall that acts as a sail.

5. Secondary Water Resistance (SWR)

Secondary water resistance is a barrier applied directly to the roof deck that prevents water intrusion if the primary roof covering is blown off during a hurricane. This is one of the most valuable credits on the form.

Rating options:

- SWR present: A code-compliant secondary water barrier is installed on the roof deck

- SWR not present or unknown: No verified secondary water barrier exists

How a new roof helps: This is where re-roofing delivers enormous value. During a re-roofing project, the contractor installs a self-adhering modified bitumen underlayment (such as GAF WeatherWatch or Owens Corning WeatherLock) or applies a spray-applied foam adhesive over the entire deck (commonly called a "sealed roof deck"). Either method creates a secondary water barrier that qualifies for the SWR credit.

The SWR credit alone can reduce premiums by $200 to $700 per year, and it is only achievable during a re-roofing project when the deck is fully exposed. This credit is virtually impossible to earn without replacing the roof.

6. Opening Protection

This section evaluates whether the home's openings (windows, doors, skylights, garage doors) are protected against windborne debris.

Rating options:

- All openings protected: Impact-rated windows/doors or approved shutters on every opening

- No protection or partial protection: Any unprotected opening disqualifies the "all protected" credit

How a new roof helps: While opening protection is not directly part of the roofing system, many homeowners choose to upgrade windows and doors during a major re-roofing project to maximize total wind mitigation savings. The opening protection credit can reduce premiums by an additional $300 to $1,000 per year depending on the home's location and insurer.

7. Existing Wind Mitigation Features

This catchall section documents any additional wind-resistant features, including:

- Reinforced concrete block walls

- Poured concrete walls

- Hurricane-rated garage doors

- Reinforced gable end walls

Maximum Insurance Savings From a New Roof

When a homeowner replaces their roof with a fully FBC-compliant system that includes secondary water resistance, upgraded deck attachment, and hurricane straps, the combined wind mitigation credits can produce dramatic premium reductions.

Savings Breakdown by Credit

| Wind Mitigation Feature | Annual Savings Range | Achievable During Re-Roof? |

|---|---|---|

| FBC Roof Covering | $400 - $1,200 | Yes (automatic) |

| Secondary Water Resistance | $200 - $700 | Yes (underlayment upgrade) |

| Roof Deck Attachment (upgraded) | $100 - $400 | Yes (re-nailing during tear-off) |

| Roof-to-Wall Connection (upgraded) | $150 - $500 | Partially (accessible trusses) |

| Opening Protection | $300 - $1,000 | Separate project |

| Roof Geometry (hip) | $100 - $300 | Only if pre-existing |

Total potential savings from re-roofing credits: $850 - $2,800 per year

10-Year Cost vs. Savings Analysis

Consider a typical Miami-Dade County home with a 2,000-square-foot roof:

| Scenario | Year 1 Cost | 10-Year Insurance Savings | Net 10-Year Position |

|---|---|---|---|

| New shingle roof + SWR + straps | $15,000 - $22,000 | $8,500 - $25,000 | -$6,500 to +$3,000 |

| New tile roof + SWR + straps | $25,000 - $40,000 | $8,500 - $25,000 | -$16,500 to -$15,000 |

| New metal roof + SWR + straps | $28,000 - $44,000 | $8,500 - $25,000 | -$19,500 to -$19,000 |

For shingle roofs, the insurance savings can recover 40% to 100% of the re-roofing cost over 10 years. Even for premium tile and metal systems, the savings substantially offset the investment. When you factor in the avoided cost of emergency repairs on an aging roof, the financial case for re-roofing becomes even stronger.

The 25% Rule and Forced Re-Roofing

Florida's 25% rule (Florida Building Code, Section 706.1.1) states that if more than 25% of a roof's total area is repaired, replaced, or recovered within any 12-month period, the entire roof must be brought into compliance with the current Florida Building Code. This rule frequently triggers full re-roofing after significant storm damage.

While the 25% rule forces an unexpected expense, it also creates an opportunity. Because the entire roof must be replaced to current code standards, the homeowner automatically qualifies for the FBC roof covering credit and can incorporate SWR, deck re-nailing, and strap upgrades at relatively low incremental cost. In this scenario, the insurance savings help offset the unexpected expense of code-triggered re-roofing.

For a deeper explanation of how the 25% rule works, see our detailed guide: Florida's 25% Roof Replacement Rule.

FBC-Compliant Materials That Qualify for Maximum Credits

Not all roofing materials are created equal when it comes to wind mitigation credits. The following materials and installation methods qualify for the highest FBC credit when installed with proper permits in Miami-Dade County:

Shingle Systems - GAF Timberline HDZ . rated for 130 mph winds, Class F Miami-Dade NOA - Owens Corning Duration STORM . SureNail technology, 130 mph rating - CertainTeed Landmark Pro . Max Def colors, 130 mph wind warranty

Tile Systems - Eagle Roofing Products concrete tiles . Miami-Dade NOA approved - Boral concrete and clay tiles . full HVHZ compliance - MCA Clay Tile . mission, barrel, and flat profiles with NOA

Metal Systems - Standing seam panels . 24-gauge minimum, concealed clip, 160+ mph rated - Stone-coated steel . Decra,DERA, Gerard profiles with NOA approval

Critical Underlayment for SWR Credit - Self-adhering modified bitumen: GAF WeatherWatch, Owens Corning WeatherLock, CertainTeed WinterGuard - Sealed roof deck (spray foam): Spray-applied foam adhesive over entire deck per FBC requirements

Extreme Roofing Inc. is a GAF Certified, Owens Corning Preferred, and CertainTeed Certified installer, meaning every roof we install uses manufacturer-approved materials and methods that qualify for maximum wind mitigation credits.

The Wind Mitigation Inspection Process After Re-Roofing

When to Schedule the Inspection

Schedule your wind mitigation inspection after your re-roofing project passes final building inspection. The final inspection verifies that the installation meets code, and the wind mitigation inspector will reference the building permit and final inspection approval as part of their documentation.

Recommended timeline:

1. Re-roofing project completed

2. Final building inspection passed (typically within 1-2 weeks of completion)

3. Wind mitigation inspection scheduled (within 1-2 weeks of final inspection)

4. OIR-B1-1802 form submitted to insurance company

5. Premium adjustment applied (typically at next renewal, or immediately upon request)

What to Provide to the Wind Mitigation Inspector

Prepare the following documents to ensure the inspector can verify all credits:

- Building permit with final inspection approval date

- Roofing contractor's certificate of completion detailing materials and methods used

- Underlayment product data (for SWR verification)

- Manufacturer product approvals (Florida Product Approval numbers or Miami-Dade NOA numbers)

- Photos from the installation showing deck attachment, underlayment installation, and strap connections

How to Submit the Form to Your Insurer

Once the inspector completes the OIR-B1-1802 form:

- Request a copy of the completed form (keep for your records)

- Contact your insurance agent and inform them you have a new wind mitigation inspection

- Email or upload the form through your insurer's portal . most Florida insurers accept digital submissions

- Request immediate review . Florida law requires insurers to apply applicable credits within 45 days of receiving the form

- Verify the premium adjustment on your next declaration page

If your insurer does not apply the full credits you believe you are entitled to, request a written explanation referencing the specific form sections. You have the right to dispute the insurer's interpretation.

HB 1305 and Post-2020 Wind Mitigation Changes

House Bill 1305 , signed into law in 2020 and refined through subsequent legislative sessions, made several changes to Florida's wind mitigation framework:

- Standardized the inspection form: The OIR-B1-1802 form is now the only accepted format statewide

- Eliminated certain stacking discounts: Some insurers previously allowed "double-dipping" on credits . HB 1305 clarified the discount structure

- Enhanced inspector accountability: Inspectors who submit fraudulent or inaccurate forms face license revocation and fines

- Clarified re-inspection triggers: Material changes to the roof (such as partial re-roofing) may require a new wind mitigation inspection

The net effect of HB 1305 is a more standardized and transparent system. Homeowners with legitimate wind mitigation features receive reliable, predictable credits, while the fraud that previously inflated some claims has been addressed.

Common Mistakes That Reduce Wind Mitigation Savings

Mistake 1: Not Getting Inspected After Re-Roofing

An astonishing number of Florida homeowners invest $15,000 to $40,000 in a new roof but never schedule a wind mitigation inspection afterward. Without the inspection, your insurer has no documentation to apply credits, and you leave hundreds or thousands of dollars on the table every year.

Mistake 2: Using an Expired Inspection

Wind mitigation inspections do not technically expire, but many insurers will not accept inspections older than 5 years. After a re-roofing project, always get a fresh inspection that documents the new installation.

Mistake 3: Not Requesting SWR During Re-Roofing

The secondary water resistance credit is only achievable during a re-roofing project when the deck is exposed. If you do not specifically request SWR-qualified underlayment, your contractor may install a standard synthetic underlayment that does not qualify. Always discuss SWR with your roofing contractor before the project begins.

Mistake 4: Skipping Deck Re-Nailing

If the tear-off reveals that the deck is attached with undersized nails, upgrading to 8d ring-shank nails costs $500 to $1,500 . an investment that generates $100 to $400 per year in insurance savings. Over 10 years, that is $1,000 to $4,000 in returns on a relatively minor upgrade.

Working With Extreme Roofing for Maximum Insurance Savings

Extreme Roofing Inc. approaches every re-roofing project with insurance savings in mind. Our process includes:

- Pre-project consultation reviewing your current wind mitigation report and identifying upgrade opportunities

- Material selection focused on FBC-compliant, NOA-approved products that qualify for maximum credits

- SWR installation using manufacturer-certified self-adhering underlayment on every project

- Deck assessment and re-nailing when tear-off reveals substandard attachment

- Hurricane strap installation on accessible roof-to-wall connections

- Completion documentation package with all product approvals, permit copies, and installation photos for your wind mitigation inspector

We have helped hundreds of Miami-Dade and Broward County homeowners maximize their wind mitigation savings since 2004. Our license (CCC# 1326021) and manufacturer certifications ensure your new roof qualifies for every available credit.

Get a Free Estimate

Ready to replace your roof and start saving on insurance? Contact Extreme Roofing Inc. for a free estimate that includes a wind mitigation savings projection. Call [305-225-1535](tel:305-225-1535) or visit our free estimate page to schedule your consultation. We serve all of South Florida from West Palm Beach to Homestead.

Frequently Asked Questions

What is a wind mitigation inspection in Florida?

A wind mitigation inspection is a standardized assessment of your home's wind-resistant features documented on the OIR-B1-1802 form. A licensed inspector evaluates seven categories including roof covering, deck attachment, roof-to-wall connections, roof shape, secondary water resistance, and opening protection. Florida law requires insurers to provide premium discounts for homes with verified wind-resistant features.

How much can I save on insurance with a new roof in Florida?

Florida homeowners with a new FBC-compliant roof can save between $800 and $2,500 per year on homeowners insurance through wind mitigation credits. The exact savings depend on your insurer, location, home value, and which specific credits your new roof earns. Over 10 years, cumulative savings typically range from $8,000 to $25,000, often recovering 40% to 100% of the re-roofing cost for shingle systems.

Do I need a new wind mitigation inspection after re-roofing?

Yes, absolutely. After completing a re-roofing project and passing final building inspection, you should schedule a new wind mitigation inspection to document the upgraded features. Without a new inspection, your insurer cannot apply credits for the new roof covering, secondary water resistance, or any other improvements made during the project. The inspection costs $75 to $150 and typically generates hundreds to thousands of dollars in annual savings.

What is secondary water resistance and why does it matter?

Secondary water resistance (SWR) is a waterproof barrier applied directly to the roof deck that prevents water intrusion if the primary roof covering is blown off during a hurricane. It is typically achieved by installing self-adhering modified bitumen underlayment or spray-applied foam adhesive over the entire deck. The SWR credit alone can save $200 to $700 per year on insurance and is only achievable during a re-roofing project when the deck is exposed.

How long does a wind mitigation inspection take?

A wind mitigation inspection typically takes 30 to 60 minutes to complete. The inspector examines accessible areas of the roof structure, attic space, wall-to-roof connections, and opening protection features. The completed OIR-B1-1802 form is usually delivered within 24 to 48 hours after the inspection. Most insurers apply the credits within 45 days of receiving the form.

Does the 25% rule affect wind mitigation credits?

Yes, indirectly. Florida's 25% rule requires that if more than 25% of a roof is repaired or replaced within 12 months, the entire roof must be brought up to current Florida Building Code standards. This forced full re-roofing automatically qualifies the home for the FBC roof covering credit and provides the opportunity to install SWR and upgrade deck attachment . resulting in maximum wind mitigation savings that help offset the cost of the code-required replacement.

Can I get wind mitigation credits without replacing my roof?

Partial credits are available for existing features. If your home already has hurricane straps, a hip roof, or impact-rated windows, those credits can be verified through inspection without any work. However, the two most valuable credits . FBC roof covering and secondary water resistance . typically require a re-roofing project to achieve. Homes built after 2002 under the Florida Building Code may already qualify for the FBC roof covering credit.

Need Roofing Help?

Whether you need an inspection, repair, or full replacement, our team of licensed roofing professionals is ready to help. Serving South Florida since 2004.

Related Articles

Florida insurance rates are dropping for the first time since 2015. Learn how combining market rate decreases with strategic roof upgrades can save Miami homeowners $1,400-$2,600 per year on premiums.

Read More

My Safe Florida Home Grant 2026: Get Up to $10,000 for Roof Hardening (Before Funding Runs Out)

The My Safe Florida Home program has $270 million available for roof hardening grants up to $10,000, but the legislature has not approved new funding for 2027. Learn how to apply and maximize your grant.

Read More